Dividends, Buybacks, or Reinvestment?

Capital Allocation 101

TL;DR Summary

Revenues tell only a small part of the picture, earnings are more important and cash flows are the real focus.

Once we are generating positive cash flows, the challenge shifts to how do we use those cash flows.

Ideally, we find productive ways to reinvest those cash flows into growing the business. Productive implies that the Return on Invested Capital exceeds the cost of capital.

Unfortunately, this is more challenging than most anticipate because it requires us to project how productive projects will be going forward. Even firms that excel at this are prone to misfires.

If a firm does not have ample opportunities to invest its cash flows productively, it should return those cash flows to investors through dividends or share repurchases.

Dividends are not tax efficient and are less flexible.

Share repurchases are often better than dividends due to tax advantages for investors, the opportunity for management to take advantage of informational edges, and flexibility.

Unfortunately, management may overuse stock buybacks and repurchase shares at inopportune times.

First, a quick housekeeping note. A couple of weeks ago, I posted a book review of Jake Taylor’s “The Rebel Allocator” and announced that there would be a winner drawn from subscribers as of August 21st. Given the relatively low number of subscribers and that probably 75% of them fall into the former colleagues, former students, and family category, it should not be a big surprise to find out that the winner was one of my former colleagues. I’ll respect his privacy and just use his first name, but Anil, I hope you enjoy the book.

Revenues, Profits and Cash Flows

One of the keys to successfully running a successful business is capital allocation — how do we direct capital to the areas where it is most beneficial to the firm. Note here that I say “one of” because there are several important keys which include, but are not limited to, hiring, developing a corporate culture, etc. Underpinning the concept of capital allocation is the idea that the firm is allocating cash flows, not revenues or (as many textbooks seem to imply) profits.

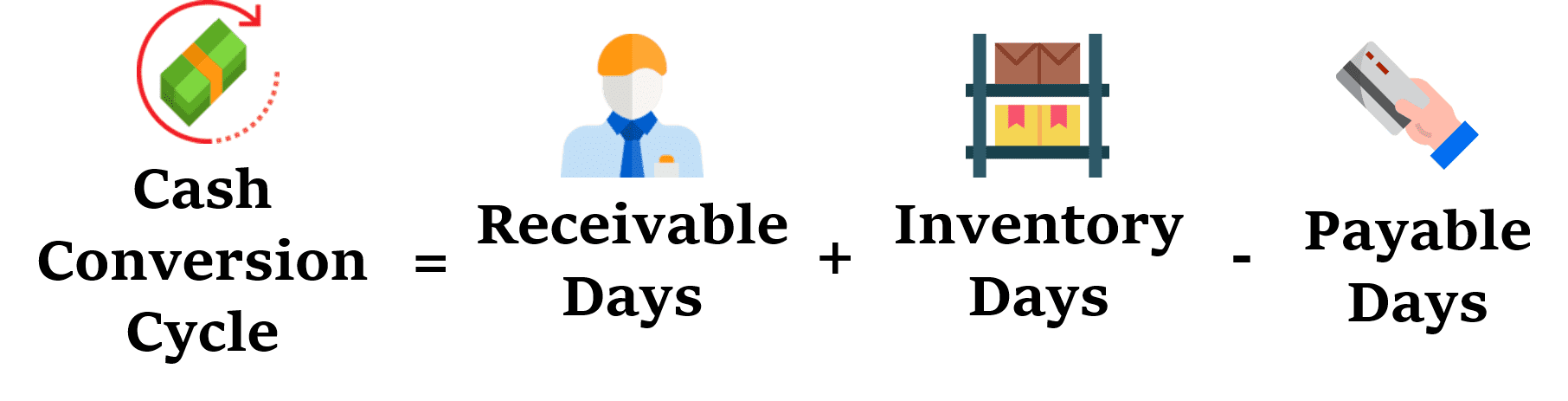

As the image suggests, revenue is potentially misleading. If my marginal cost of manufacturing/distributing my product is $100 and I sell it for $90, higher revenues are actually damaging. If I sell it for $100, revenues are irrelevant. If I sell it for more than $100, the relevance depends on how many I sell and how much above $100 I get. Maximizing revenue is a distraction, not a legitimate goal. Profit is better, but profitable firms can go bankrupt without cash flows. That is because companies use accrual accounting rather than cash-based accounting.1 This means that revenues are recognized as they are earned (not when actual cash payment is received) and expenses are recognized as the revenues are earned as well. Consider a company that needs a lot of inventory which is paid for at the time the inventory is purchased and sells their product on credit. There can easily be a couple of months between the time the cash is paid for the inventory and received from customers (this is the cash conversion cycle).

Even worse, if the company is growing at a fast enough pace it is likely spending more money on additional inventory, production facilities, employees, etc. and may be “profitable”, but burning through cash. This is why (especially for smaller firms with less access to financing), rapid growth can be problematic.

That said, let’s assume that for our generic firm, profits and cash flows are equivalent2 and the firm is profitable to the extent that it generates more than it needs to cover replacement-level capital expenditures.3 Therefore, this firm needs to figure out the optimal way to invest in growth or return capital to shareholders.

Capital Allocation

The first question that should come up is two-fold. First, how much capital do we have to reinvest, and second, how many good opportunities do we have to reinvest that capital? The first question is relatively easy (although can get a little more complex due to capital structure — the mix of debt vs. equity financing — issues). The second is MUCH trickier. Companies can

Reinvest in their core product lines. For example, Walmart can build new stores, new distribution centers, etc.

Expand into adjacent areas. For example, Netflix went from renting DVDs via mail, to streaming content licensed from other parties, to developing their own content to stream.

Acquire other companies. Facebook famously “overpaid” to acquire Instagram for $1 billion in 2012. Given that by 2018, Instagram was estimated to be worth over $100 billion, maybe they didn’t do quite as bad as critics of the deal initially thought.

Move into new areas to seek growth or opportunities. Berkshire Hathaway owns insurance companies (GEICO), a railroad (BNSF), an energy company (Berkshire Hathaway Energy — 90% owned), a candy company (See’s Candies), and others. These companies were acquired as they appeared to be attractive investment opportunities.4

A challenge to each of these strategies is that it is just as easy to present horror stories. Consider that Amazon, who hit a home run and then some with their investment into their AWS cloud platform (generating revenues of $45 billion in 2020), also developed the Fire Phone which was a complete flop. Disney, who introduced us to the Marvel Cinematic Universe and Disney+, also produced The Lone Ranger in 2013. How bad was The Lone Ranger? Disney expected to take about a $150-$190 million dollar loss!

Ideally, companies would invest in projects which have a positive net present value (NPV).5 Unfortunately, (remember last week’s piece on false precision) that is only an estimate, as it requires us to forecast what will happen in the future. Disney didn’t produce The Lone Ranger expecting to lose over $150 million. Investors can try to look at the company’s previous track record by considering their Return on Invested Capital (ROIC) or Return on Incremental Invested Capital (ROIIC) and comparing it to the company’s cost of capital. If the ROIC or ROIIC are larger than the firm’s cost of capital, that is a sign that (at least historically), the company has made good investment decisions. Note that even companies who excel at capital allocation will have a few misses, so it is important to look at their track record over time. Then, and this is the tricky part, investors need to consider (a) does the company have more opportunities that they can take advantage of, (b) how successful will these opportunities be, and (c) do they have enough good opportunities to use all of their profits? Value for investors is only going to be produced when companies have more or better opportunities than investors have priced into the stock. Finding companies run by management teams that excel at identifying quality investment opportunities is therefore an essential element in evaluating potential investments. This is sometimes referred to as optionality — having multiple different alternative future investments based off of what we are doing now.

Returning Capital to Investors

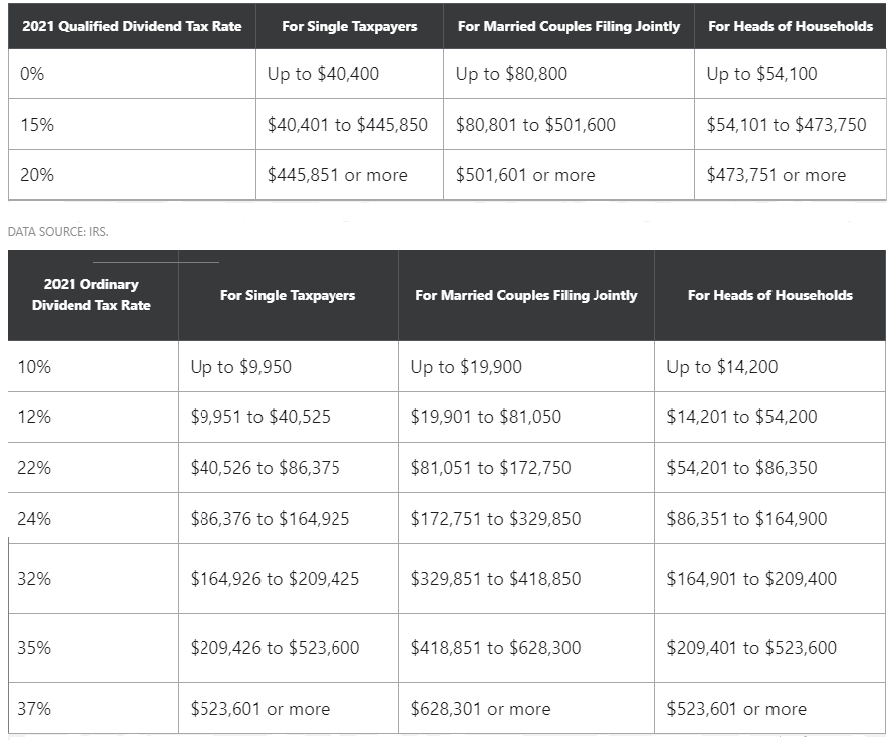

If the firm does not have enough projects to invest in, they should return the excess capital to investors. There are two primary tools with which to accomplish this — dividends or stock buybacks.6 Dividends are taxable and the rules are a little complex. If you own shares in a tax-sheltered account, the impact of dividends ranges from not relevant now to not relevant at all.7 If you own shares outside of a tax-sheltered account, it looks like this:

So, if you are married, filing jointly with $100,000 in income, earning a 3% dividend yield will either give you a 2.55% yield assuming they are qualified dividends (which is the most common situation) or 2.34% yield if they are not. While that may not seem like a big deal as you are only losing 0.45% or 0.66% of your return, over a 35-year time horizon with $500/month, that would total $156,853 or $223,649 less wealth (assuming a 9% return before taxes).

The last way to return capital (at least without getting into more complex financial engineering) is for the company to buy back shares of stock. In 1982, the SEC introduced Rule 10b-18, which essentially allowed firms to start buying back shares of stock without getting into regulatory issues assuming they meet some general requirements. While this had little impact initially, by the late 1990’s, stock buybacks started to be used more frequently as a way to return capital to investors.

The general idea is that if the firm has 1,000,000 shares of stock outstanding and buys back 100,000 of those shares, this increases the value per share.8 However, this creates a better tax situation for investors because the increase in value per share becomes a capital gain (which only become a taxable event when the investor sells the shares). Therefore, an investor can defer capital gains by just choosing not to sell.

Another potential benefit occurs if we believe that management has asymmetric information regarding the value of the company. With buybacks, the argument is that management may feel that the stock is worth $100 per share (again, they don’t KNOW it is worth $100, but may have a better idea of the firm’s opportunities/strategies/ competitive/etc. positions than the marginal investor). If the stock is trading for $70, a buyback generates an immediate value generation of $30 per share. This is on top of the slight tax advantage. If the stock is trading for $120, then a buyback is going to waste $20 (which is going to far outweigh the tax advantage). If you believe management has asymmetric information and can use it correctly, buybacks create an advantage.9

One last benefit of buybacks, relative to dividends, is that buybacks create a little more flexibility. When firms cut dividends, it is generally seen as a sign of financial distress. Buybacks, alternatively, are typically instituted over a time frame. For example, here is Berkshire Hathaway’s share repurchase (buyback) strategy from their 2020 10K

Berkshire’s common stock repurchase program permits Berkshire to repurchase its Class A and Class B shares at any time that Warren Buffett, Berkshire’s Chairman of the Board and Chief Executive Officer, and Charles Munger, Vice Chairman of the Board, believe that the repurchase price is below Berkshire’s intrinsic value, conservatively determined.

Here is Altria’s repurchase program

In January 2021, the Board authorized a new $2.0 billion share repurchase program, which Altria expects to complete by June 30, 2022. The timing of share repurchases under this program depends upon marketplace conditions and other factors, and the program remains subject to the discretion of the Board.

Note that both of these programs have flexibility built in.

In general, capital allocation implies the firm trying to best use the firm’s capital in order to generate value for shareholders. Ideally, the firm has a long runway of projects with high ROIC/ROIIC that exceed their cost of capital, in which case they should be pursuing these instead of paying dividends or repurchasing shares of stock. Investors will benefit from finding firms run by management who excel at finding these situations. Note that this is easier than said than done, as past records are a function of both skill and luck. Also, the environment that they have been operating in is constantly in flux. Finally, how do we know what will happen if there is a change in management? All of these introduce risk. After that share repurchases are often better than dividends (especially for investors who are not able to take advantage of tax-sheltered investment accounts).

There is good reason for this based on the “going-concern” concept which argues that a firm is not just being managed for the current period, but as if it will be around for the long-term. The downside is that it requires the firm to remain solvent over the short-run.

They aren’t, but they probably move in the same general direction most of the time.

In other words, think of a firm that is spending enough to replace their assets that are wearing out. However, it is not spending on future growth opportunities and merely maintaining their “going-concern” status at its current level.

Note that this is not a current list of all Berkshire holdings (which change regularly), but instead a snapshot of what the company looked like at one point in time. As of June 30th, Berkshire’s largest 10 holdings (by market capitalization) are Apple Inc., Bank of America Corp, American Express Company, Coca-Cola Co., Kraft Heinz Co., Moody’s Corporation, Verizon Communications Inc., US Bancorp, BYD Co. Ltd, and DaVita Inc.

Net present value is a finance term which essentially estimates the present value of all the expected cash flows from the project (both positive and negative) discounted back to the project initiation point at the appropriate risk-adjusted discount rate.

For clarity here, when I talk about stock buybacks, I’m referring to buybacks that actually reduce the number of shares outstanding. Often firms use buybacks to acquire shares which are used as stock-based compensation. This is not really returning capital to investors and just offsetting the dilution in shares created by stock-based compensation.

Dividend taxes can get a little tricky as dividends can fall into two categories — qualified or ordinary. The tax treatment is different depending on which category the dividend falls under. Qualified dividends refer to dividends from most common shares and are taxed similarly to long-term capital gains. Dividends on REITs and Master Limited Partnerships or for stocks held only a short period of time are ordinary dividends and are taxed at ordinary income rates. If you hold your shares in a Traditional IRA/401(k), you will eventually pay taxes when you withdraw your income (hopefully years or decades from now), whereas if you hold your shares in a Roth IRA/401(k), you will not pay taxes when you withdraw.

Again, assuming that the company is actually reducing the shares outstanding.

The flip side is that, like virtually everyone, management probably suffers from the optimism bias which will cause them to tend to be more optimistic about the firm’s prospects than they should be.