The Rebel Allocator (Book Review)

Value Exceeds Price

This week, I’m going to do a book review of The Rebel Allocator by Jacob L. Taylor. Yes, this is the same Jake Taylor whose tweet was the inspiration of last week’s post.

As a bonus, anyone who subscribes to this newsletter by 12:00 PM CST on August 21, 2021 will be entered into a drawing for a free copy of The Rebel Allocator (you’ll have to provide a mailing address if you are selected as the winner or I can send a Kindle version if you prefer).

One of my favorite podcasts is Value: After Hours1 with Tobias Carlisle, Bill Brewster and Jake Taylor (and occasionally Michael Mitchell). Jake is famous for providing the “veggies” in the podcast, which are often little segments from nature that he uses as analogies to provide a different way to think about investment strategies. I provided a bit of a background on Jake last week, but figure it can’t hurt to throw in a quick recap. In addition to being a host of VAH plus Five Good Questions podcasts and CEO of Farnam Street Investments, Jake has also written a book called The Rebel Allocator.2 This book is an interesting twist on the concept of writing some guidelines for capital allocation in that it is fiction. As with most endeavors, there are some highlights and lowlights, but fortunately more of the former and relatively few of the latter. As I’m sure you’ve guessed, I have a lot of respect for Jake’s perspective, so this is not a 100% unbiased review.

Our heroes of the story are Nick and Francis Xavier (aka “Mr. X”). Nick is a journalism graduate who is starting a career in investment banking. Mr. X is a billionaire business tycoon passing on his business knowledge to Nick, who is tasked with writing Mr. X’s dying biography. During the process, Nick goes from looking to uncover Mr. X’s dark secrets of exploitation (you don’t get to be a billionaire without exploiting society, right?) to discovering that business creates value by serving society. While my response in the classroom for years when students would ask a question on a topic like this was often “it depends” (as the world is rarely a binary good vs. evil dichotomy), I tend to side with the point of view that capitalism is an imperfect system that creates a lot more good than bad. Your mileage may vary.

Is it a good book? I’d give it 4 out of 5 stars3. Your take on the book will probably depend on how much you appreciate the business views of Warren Buffett and Charlie Munger as they are clearly the models for Mr. X (great models from my perspective) and your views on using fiction as the basis for delivering business lessons. No offense to Mr. Taylor, but I don’t think he’s quite ready to win any awards in the field of fictional writing (and I doubt that was his intent either). Then again, I am hardly qualified to play critic in the realm of fiction as my tastes tend to run towards generic thrillers (c’mon, who doesn’t love a good Joe Ledger story) and books by Stephen King. I will say that I did enjoy the concept of using a fictional story to illustrate lessons on business and capital allocation. While it lacked some of the interesting stories and anecdotes that one gets in a non-fiction version, it may be more approachable to people who view non-fiction as too similar to being in “school.”

As for the business advice, I thought most of it was done quite well. Some of the topics have come up in the VAH podcast (such as yarak – a falconry term focusing on an optimal state of hunger for hunting), but the tool that I found most intriguing was using straws to break down concepts such as cost, price, and value into multiple “lessons” for the reader. A simple concept that for a business to thrive, it must sell its product/service for more than the cost to produce it (or there would be no profit) and the consumer must feel that the value being received is greater than the cost (or there would be few customers). The more value exceeds price, the greater the brand equity that is being built up.4

While one might think that the optimal strategy than is to lower cost, that is incorrect because if you focus only on minimizing cost, you destroy the value. In addition, the concept of fixed vs. variable costs are explored in this manner. Mr. X’s business empire is built around Cootie Burgers. The fixed cost (such as the building for restaurant) is, for the most part, not a function of the number of burgers sold. However, if they serve 10% more customers, the fixed cost per burger drops. By using the three straws to represent three key themes, the author allows Mr. X to teach Nick (and thereby the reader) many issues related to how cost, price, and value impact business decisions.

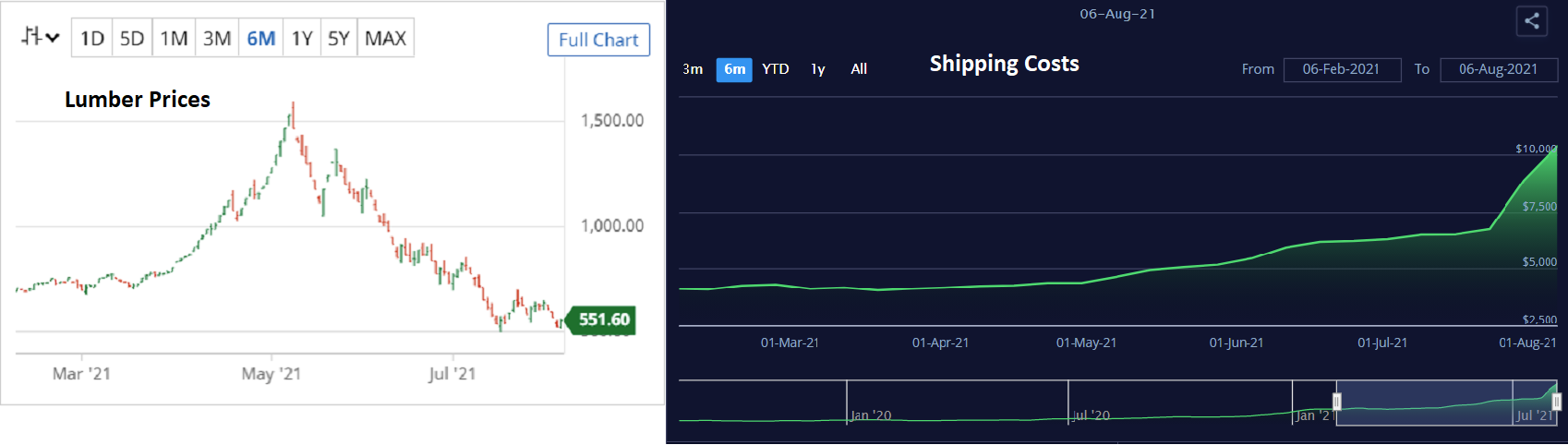

On the flip side, there is an important distinction from broad concepts to applying those concepts. How does one adjust the concept for shocks to cost (for example, the recent runup — and back down — in lumber on housing costs, or the increased shipping/freight costs),

impacts of pricing power due to competition/technology (how would the entertainment world be different if Blockbuster had purchased Netflix for $50 million in early 2000?), differing value propositions (I may value a ticket to the next Marvel superhero film at $30 and you may value it at $5 — how does Disney determine the price to maximize their brand?), or the role of luck (in our story, Nick meets Mr. X by winning a drawing…what if he didn’t win?). These details are what move us from concept to application and are much harder to incorporate into the decision process than most would like to acknowledge. Granted, these are well beyond the scope of the book (as I’m sure that Jake would agree) but they are questions to think about in implementing the lessons.

There are some other lessons that I found less effective. For example, the concept of franchising came up and there are many pros of the franchise model. Domino’s Pizza has excelled with their franchise model over the past 10 years and rewarded shareholders tremendously (almost 40% annual returns from 2011-2020) with a franchise model. Conversely, Chipotle has avoided franchises and also done quite well (despite some food safety issues in the middle of the decade) with just over a 20% annual return during that same time frame.

In the book, Mr. X discusses that franchising allows them to focus on what Cootie Burgers does well (operations) and not on real estate. This is a valid point. However, it also creates one more layer of separation between Cootie Burgers and the franchisee running the franchise. While this can be managed, it does require additional focus on doing so. In a similar vein, there is a discussion of how a food truck can be used as a way to scout locations for new restaurants at a much lower cost. However, it is not clear that the food truck experience and the restaurant experience overlap enough to assume that a profitable location for the food truck would be a profitable location for a restaurant.

The ”educational” aspect of the book was worth the cost of admission (value greatly exceeded price). Note that when I refer to the educational aspect, I’m not just talking about taking ideas at face value. Regardless of whether or not a book is fiction or non-fiction, it is telling the author’s story. It is wrong to assume the author does not have biases, is accurately describing the “truth” (and truth is in quotes because often the truth is a lot murkier than we’d like to believe), or that what is assumed by most to be valid today will be assumed to be valid next year or next decade. Knowledge evolves by questioning that knowledge. Therefore, even things that I see as a weakness (such as can a food truck predict the appropriate location for a restaurant) may just be opportunities for debate. And, shocking as it may be (he says sarcastically), I may be the one who is wrong. However, I think part of the reason I enjoyed the book was seeing Mr. Taylor take on the risk of presenting it in a fictional setting. Whether that works for you or not is going to come down to personal preference, but I applaud the bold choice.

I also like the overall theme. Capitalism is not inherently evil. The process of earning profits over time by providing consumers situations where their perceived value exceeds the cost of what they are purchasing is an essential tool for making consumers happy. Does capitalism have flaws? Yes, as do all economic systems. However, making business owners happy often is a function of making consumers and employees happy.5

The link is to YouTube, but you can also download the audio podcast from just about anywhere you get podcasts

If you, like me, are a fan of Jake’s work, let me recommend his quarterly letters to Farnam Street investors.

Note that relatively few books would get 5/5 stars (probably less than 10%), so 4/5 is a strong rating. A few that come to mind would be Range: Why Generalists Triumph in a Specialized World by David Epstein, Thinking in Bets: Making Smarter Decisions When You Don't Have All the Facts by Annie Duke, and The Psychology of Money: Timeless Lessons on Wealth, Greed, and Happiness by Morgan Housel.

This diagram was introduced on p. 68 and minor variations of it were used multiple times throughout the book as Mr. X taught Nick lessons. For example, if price is below cost, the firm is likely heading into bankruptcy. If price is greater than value, the customer will feel cheated. It is a simple, but powerful visual tool for illustrating some essential concepts.

Not the key disclaimer there…”often”. There are situations where monopolies exist, competition is throttled due to regulatory or market structure issues, externalities distort the price/cost relationship, and promotors intentionally mislead investors/consumers about goods/services/investments (among other issues). This is why regulations are needed and the appropriate debate is at what level the regulations enhance or distort ability to efficiently allocate capital for the benefit of society.