Expectations and News Events

What Drives Stock Prices -- Turning Point Brands and Tesla

Before we dive into the main topic for this week, I want to take a moment to make a pitch for subscribing to David Epstein’s Range Widely newsletter. It’s free (gotta like that price point) and you can find this week’s excellent piece titled “TikTok Tourette’s” here. It’s about a 5-10 minute read with a really interesting topic of how mental stress can lead to physically “contagious” symptoms. And the quotes around contagious are not meant to be sarcastic, instead it seems as if the brain latches onto others behavior as a stress release valve and imitates it. If you’ve heard of mimetic behavior (which is indirectly touched on later in my piece this week with Tesla discussion), you’ll recognize this as one of the characteristics. Check it out.

Last week was a big earnings reporting week for the financial markets as Amazon, Apple, Facebook and many more reported their 3rd quarter earnings for 2021. Whether it is an earnings report or other news, such as Hertz agreeing to buy 100,000 new Tesla’s by the end of 2022, news events have a big impact on stock prices.

A quick, but essential note. I write this during the week and usually use Tuesday’s for touch-ups and final edits. I’m not rewriting this week’s edition because (1) the content is still valid and (2) while the “news” changed, it captures the somewhat random nature of news flows pretty accurately. That said, I wanted to address a late-breaking, important news update. On Monday evening (after most of this had been written), Elon Musk tweeted out the following:

So, the news that added over $300 BILLION in value to Tesla in 6 trading days as the stock went from $909.68 to $1208.59…may be irrelevant. This ties into some of my discussion later about the promotional aspect of Elon Musk. You might ask why it took him a week to make this statement, but if so you do not understand the way Elon’s mind seems to work. You might also note that between the time the announcement was made and Elon’s tweet, Tesla increased its stock’s value by nearly 33% and then fell by 3% on Elon’s statement that there is no contract and the Hertz deal has no effect on their economics. Carry on.

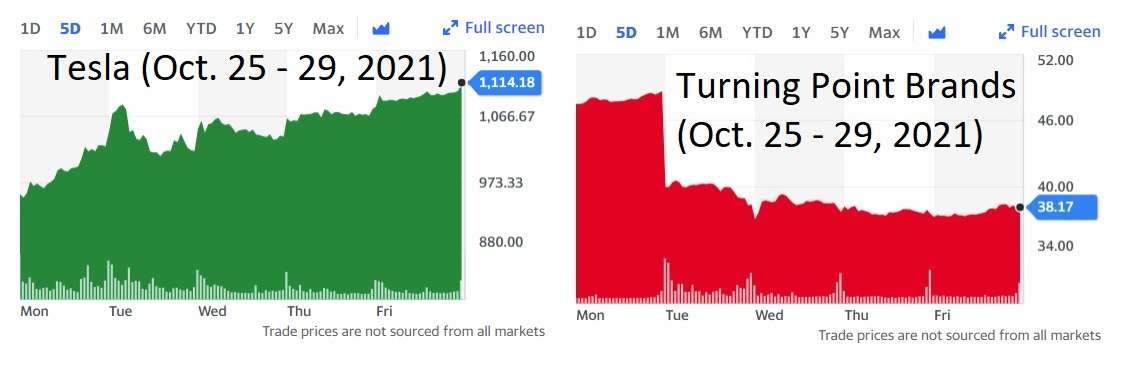

Which introduces today’s topic of how and why news drives stock prices in ways that are not always intuitive. Here is a chart that looks at two companies from last week — Tesla and Turning Point Brands.

Let’s start with Tesla. Tesla closed the previous week at $909.68 before rising to $1114.00 at the end of the week. This represents a gain of $204.32 per share or about 22.4%. Given that Tesla has 1,123 million shares outstanding, this represents an increase in the total value of Tesla shares of $229 billion dollars. For perspective, the market capitalization of Ford right now is about $65 billion. Alternatively, if you prefer enterprise value (essentially the value of all the equity and all the debt) for Ford, that is about $172 billion. In other words, Tesla’s value for the last week exceeded the total value of Ford.1 This huge increase in Tesla’s value was driven (HA! See what I did there?) by Hertz agreeing to buy 100,000 Tesla Model 3s for a total of about $4.2 billion. If you are wondering how $4.2 billion in additional revenues (not profits), you are not alone. We’ll come back to that in a bit.

How about Turning Point Brands? If you aren’t familiar with TPB, they are a tobacco company probably most well known for their Zig-Zag rolling papers which are expected to benefit from the increased rollout of cannabis.

Turning Point Brands had their earnings announcement on Tuesday, Oct. 26th before the markets opened. They reported that net sales increased 5.5%, gross profit was up 12.3%, and net income was up 49.3%. This resulted in just over a 20% DROP in the stock’s market value.

How does a company report improved sales and income only to see their stock price get flattened like it just got run over by a hurricane? The answer lies in expectations. News can not be looked at in isolation. Instead, it needs to be evaluated relative to what was expected.

Report Card Analogy

Imagine you and your good friend are back in sixth grade and it is report card time.2 You are a great student and have gotten all As for the last couple years. Your friend is not as good of a student and has gotten a steady stream of Cs for the last year. However, this time, you get 3 As and 2 Bs on your report card. Your friend got 3 Cs and 2 Bs on his report card. When you show your report card to your parents, they ask what was wrong. Were classes harder? Were you not studying as much? Is there anything causing you to be distracted. On the other hand, your friend’s parents are encouraged by his 2 Bs. Congratulations on the improvement, they say. Good work, we should go celebrate. Why are you getting concern and your friend is getting praise when you did better significantly better than him? The answer lies in expectations. You’ve established a track record that has your parents expecting As, so the 2 Bs are concerning to them. Your friend has established a track record that has his parents expecting Cs, so the 2 Bs are a sign of improvement. We aren’t evaluated on our raw results, but on our performance relative to expectations. This is true in academic performance, athletics, careers, personal attributes and just about everywhere. It is also true in the investment world. We can only determine if the news is good or bad AFTER we know what the consensus expectations were.

Returning to Turning Point Brands

If Turning Point Brands, exhibited growth in sales and earnings, why did their stock drop? The key is forward guidance — essentially the expectations that they are providing to investors for the rest of 2021. Here is a quote from their 3rd Quarter Conference Call:

With that backdrop we updated our 2021 guidance as follows: Net sales of $433 million to $443 million. This is compared to previous guidance of $447 million to $462 million. This range is unusually wide for this point in the year given the limited visibility in the vape regulatory landscape. Adjusted EBITDA for the full year is now expected to be $104 million to $108 million with the previous guidance of $108 million to $113 million.

In effect, they are expecting net sales for the year to come in 3.1% - 4.1% lower than previously thought. In addition, and probably more importantly, their adjusted EBITDA is expected to be about 3.7% to 4.4% lighter than previously thought. This is primarily a result of regulatory issues around their vaping products (NewGen).

That is still a far cry from explaining a 20% drop in the stock price. However, we need to remember that investors are also risk averse and this uncertainty raises the potential risk. Part of the risk is the question of “How reliable is management guidance?” Here is the first question from the conference call by Vivien Azer:

So I think we should start with the guidance. The market is clearly taking down the stock more than the implied percentage reduction to your revenues and EBIT, which clearly tells you that the problem isn't just with the guided revision, but kind of how the year I think has been telegraphed thus far.

This essentially is asking management why their outlook was so positive in their 2nd Quarter report and now much more cautious. Is the 20% drop an overreaction or are there some real problems that were discovered in the quarter? This is a question that the markets will decide over the next few years. For the record, I do own a bit of Turning Point Brands in my portfolio, but it is a relatively small position. Most of my positions are under 2% of the portfolio and this one is closer to 1%. While not exactly my favorite news of the day, this did not make me decide to sell the position.

Tesla Revisited

Tesla is one of the more controversial stocks in the market with strong opinions on both sides. I’m pretty sure if you gathered Tesla bulls and bears into the same room to discuss Tesla’s outlook, it would look something like this

Part of it is Elon Musk, who is alternatively seen as either the brilliant genius who is going to use his knowledge, willpower and force of personality to help mankind or as a snake-oil salesman who is duping customers and shareholders to help boost his ego and bank account. There is some truth to both of these points of view, but neither is likely accurate either. Regardless of how famous and successful people are, virtually all are (like most of us) complex, with both good and bad traits.3 The reality though is that his personality and popularity have probably bought Tesla opportunities that other companies would not have had. Like Apple products, Musk has managed to make owning a Tesla a status symbol that has value to customers as it becomes part of their identity. This is not different than Supreme, Rolex, Hermes and other brands which are owned less for their utility and more for their ability to note wealth, style, and taste. They have captured the mimetic quality that allows one to signal to others that you are part of a cooler tribe.

Another part is the significant lead that Tesla has developed in the electric vehicle (EV) market. While there are other players in the industry, Tesla is by far the dominant force at the moment. Here are some stats from 2020:

All-electric car sales in Q1-Q4 2020:

Tesla: 499,535 (23% share)

SAIC: 243,201 (11% share)

Volkswagen Group: 227,394 (11% share)

Renault-Nissan-Mitsubishi Alliance: 172,673 (8% share)

BYD: 131,705 (6% share)

Top 5 total: 1,274,508 (59.5% share)

others: 866,803 (40.5% share)

Total: 2,141,311

This, combined with the promotional nature of their CEO Elon Musk, creates significant mindshare advantage for Tesla. Statista rated Tesla’s brand value as worth $42.6B as of August 2021, 58% higher than runner-up Toyota and over 300% more than Ford.

Another advantage, which I would argue again is related to the promotional strategy of Elon Musk, is that Tesla’s advertising spending is essentially zero.4 Ford, on the other hand, spent $2.8 billion in 2020 after spending $3.6 billion in 2019 and $4.0 billion in 2018. To put that in perspective, Ford’s advertising budget for the last three years accounted for $10.4 billion and their free cash flows for those same three years were $35.8 billion — advertising (at least pre-tax) ate up almost 30% of their free cash flows which creates a significant advantage for Tesla.

What helped Tesla’s stock climb so much was the promotional nature of the news that enhanced the perception (right or wrong) that Tesla is the leader in the EV market. Stock prices are based on the present value of discounted free cash flows that the firm will generate. If a story raises the expected free cash flows (key being expected as no one has the magic crystal ball that provides the actual free cash flows), this will increase the market value of the stock. Expectations for Turning Point Brands were lowered and the stock price followed them down. Expectations for Tesla were raised and the stock price followed that up.

Predicting Stock Returns is HARD

Does this mean Tesla deserves their valuation? No, not necessarily. Personally, I would give an emphatic NO. However, I’ve learned that my ability to predict the future is probably about as good as the average human. Which means, not good, but better than a chimpanzee.5

In other words, my views on Tesla have been wrong for quite awhile (much like my views on Bitcoin and other cryptocurrencies), and there is no strong reason to assume I will be “right” over the next year. This is why I am of the opinion that a well-diversified, low-cost, tax-advantaged portfolio is essential to one’s financial health. There IS a place for picking individual investments, but that place needs to be considered with a recognition that predicting stock returns is really, REALLY hard and you are likely to be wrong often.6 One of the easiest ways to be wrong is to forget that the people on the other side of your trade are not likely to be buying/selling randomly. Instead, they are also trying to predict the stock returns and have reached a different conclusion. Therefore, in order to have an advantage, it is essential to think about what the consensus outlook is and why your outlook is different. Make sure you understand the alternative case and can make a valid argument against it. That does not guarantee you will be right. However, buying and selling stocks based only on your outlook in isolation is a lot like playing poker and ignoring the information you can receive by the betting patterns of your opponent. While they will try to disguise their betting patterns to make them less predictable, when someone has folded their last 15 hands and then plays aggressively, your view should be different than when someone has raised in 10 of their last 15 hands. That information is less reliable for this hand, but ignoring it is a sure way to become the sucker at the table.

Technically, they added about 1.33 Ford’s to their value.

It’s been awhile since I’ve gotten a report card, so I’m assuming letter grades are still standard with A, B, C, D and F. If not, just go with me on this one.

Yes, I’m sure that there are exceptions, but few people are purely evil…even politicians.

You could make an argument that their promotional expenses are in some effect advertising and I would not disagree. However, according to their 2020 annual report “Marketing, promotional and advertising costs were immaterial for the years ended December 31, 2020, 2019 and 2018.”

According to Don Moore, a professor of organizational behavior at UC Berkeley’s Haas School of Business — “Yeah, we don’t do a perfect job of calculating future benefits and losses. On the other hand, we’re a whole lot better at it than chimpanzees.”

LibertyRPF recently made the case on Jim O'Shaughnessy’s Infinite Loops podcast that the intangible benefits of learning made individual stock selection worthwhile — “I'm learning every day, so that intangible stuff has so much value to me. How many percentage points of returns is that worth? If I could do 12% in an index, I'm doing 10%, but I'm having a great time, I'm meeting great people, to me, that's worth millions, right?”