Tax Sheltered Investments

Keep More of What You Earn

Disclaimer — This is designed as general information and is NOT tax/investing advice. Please consult your financial advisor and/or tax professional for personalized advice.

TL;DR Summary

Tax shelters such as Individual Retirement Accounts (IRAs), 401(k)/403(b) plans, etc. allow investors to keep their returns instead of paying taxes.

Traditional tax shelters create an immediate tax benefit (you get a tax benefit for your contribution when you make it), allow your returns to compound tax-free for as long as it remains in the tax shelter, but require you to pay taxes on withdraws during retirement.

Roth tax shelters do not offer an immediate tax benefit on your contribution, but still compound tax-free for as long as it remains in the tax shelter, and do NOT require taxes when withdrawn during retirement.

Assuming someone was earning $60,000 per year, received a 50% match on 6% of their 401(k), contributed $250/month to a Roth IRA earning 8.5% per year and averaged a 13% tax rate on investment income for 37 years would have $2,170,528. The same out-of-pocket savings, ignoring any tax shelter tools, would come to $1,276,132.1

Compounding in a tax-free environment allows your investment snowball to grow faster, which significantly increases your wealth over time. In the example above, the increased wealth comes both from the employers match (the $1800 per year contributed by the employer created about $350,000 of the additional wealth) and the tax benefits (which contributed a little more than $540,000 of the additional wealth).

The risk/return profile of your tax-sheltered investments depends on how you decide to invest. Typically, higher risk investments will generate higher returns over time, but there is no guarantee on this (especially over shorter 5-10 year time frames) otherwise it would not be higher risk.

You might have heard the recent story about how billionaire Peter Thiel invested just under $2000 into a Roth IRA in 1999 and it grew to $5 billion in 2019. The key to this is that he put in 1.7 million founder shares of Paypal valued at $0.001 per share in January of 1999. By the end of 2002, Thiel’s Roth IRA was valued at $28.5 million…not a bad return! Another impressive IRA story, mentioned in the same ProPublica article linked above is Ted Weschler, who works for Berkshire Hathaway and grew his IRA into a value of over $250 million. Mr. Weschler, though, accomplished this without taking advantage of non-public shares. Instead, compounding returns at approximately 30% rates over multiple decades was his secret sauce. These stories are outliers (one of which I would argue may obey the letter of the law, but not the spirit of it). Saying “Well, if Ted Weschler can compound returns at 30% per year, so can I” is essentially the same as saying “Well, if Giannis can score 28 points per game and grab 11 rebounds in the NBA, so can I.” However, tax-sheltered investments such as IRAs, 401(k), and 403(b) plans are powerful tools which YOU can use to create a comfortable retirement.

Retirement plans are split into defined benefit plans and defined contribution plans. The defined benefit plan refers to the old-school pension plan where the employer promises retirement benefits to employees based on their time of service and what they earned while working. This places the risk of the plan (how long employees live to claim retirement benefits, returns on the pension assets, etc.) on the employer. Defined contribution plans flip this so that the risk is on the employee. If the employee doesn’t save enough, generates poor returns, etc., that impacts the employee. In a company sponsored plan (such as a 401(k) or 403(b) plan), the employer will often contribute a matching component to aid the employee’s savings. However, the performance risk and need to contribute are still on the employee. Individual Retirement Accounts (IRAs) are similar, but remove the employer from the process. There is no employer matching component or employer involvement at all, but instead just a relationship between the individual and financial institution acting as the custodian.2

Most employers offer something equivalent to a 401(k) plan (a 403(b) plan is essentially the same thing as a 401(k), but is offered by non-profit or government organizations). According to a recent (2016) survey, over 100 million people in the US were participants in a 401(k) plan, a number which has probably grown since then. 401(k) plans were introduced in 1978 and started to become mainstream in the early 1980’s. Because 401(k)/403(b) plans are offered through an employer, they often come with additional aspects such as “matching” contributions and vesting requirement. The match refers to how much the employer adds. While matching policies vary from one employer to the next, the most common match is typically 50% of 6% of the employees income. Therefore, if you make $50,000 per year, 6% of your income is $3000. If you contribute $3000, your employer would also contribute $1500 as their match, allowing you to save $4500. As the match is a benefit to the employee, there is often a string attached in how long you must work for the employer in order to get to keep the benefit when you leave. This is referred to as the vesting policy and will typically be 1-5 years. When you are “cliff vested” this means there is a specific time that the employer’s match switches from not yours to 100% yours. A graded vesting plan moves a certain percentage of the employer’s match to yours (for example, you may be 20% vested after 1 year, 40% vested after 2 years, etc.). Once you are vested, all future employer contributions are automatically yours.

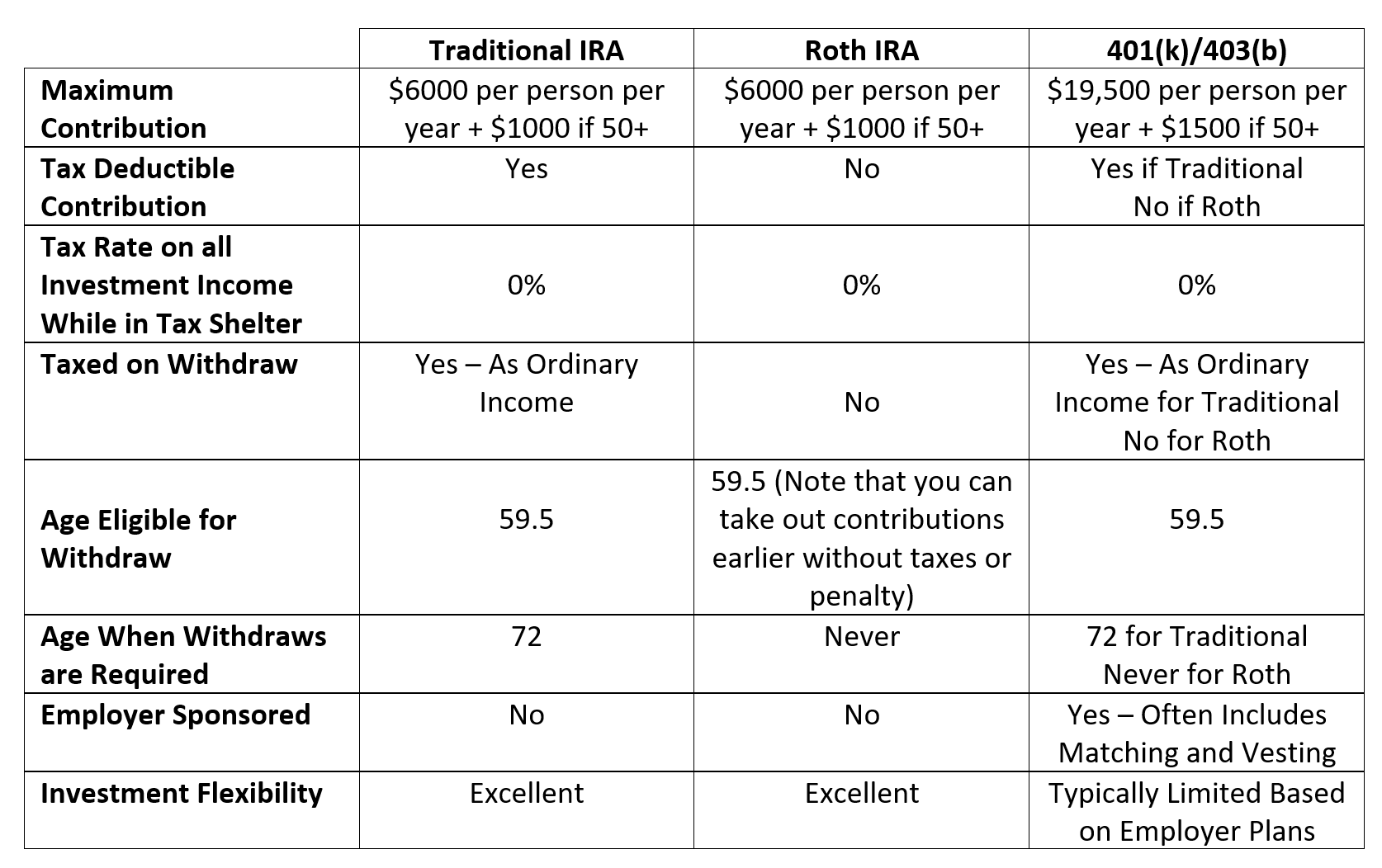

Maximum contributions to a 401(k)/403(b) plan are $19,500 per person with an additional $1500 per year allowed for those 50+.

Individual Retirement Accounts (IRAs) were created in 1974 with the Employee Retirement Income Security Act.3 When the IRA was created, it was only available for people without pension plans at their work. In addition, they were limited to $1500 per person per year until 1981 and non-working spouses were not eligible until 1977.4 Since then, there have been several improvements in the IRA system, including:

Raising the normal contribution to $6,000 per person per year (including for a non-working spouse)

Allowing a $1000 additional “catch-up” contribution for those 50-years of age or older.

Introducing the Roth IRA in 1997 which offers a back-loaded tax benefit instead of front-loaded (withdraws from the IRA are tax-free, but you don’t get a deduction on the contributions) along with a few other differences.5

Below is a table which highlights some of the key attributes of traditional IRAs, Roth IRAs, and 401(k)/403(b) plans.

Remember that the three levers to building wealth are time, rates of return, and saving. These tax shelters fall under the rates of return. One common question that I received when teaching finance classes was “How much can I expect to earn on an IRA/401(k)?” While you’ve probably heard the phrase “there are no stupid questions” (spoiler — there are), this is a case where it is the WRONG question. The reason I say it is the wrong question is that an IRA, 401(k) or 403(b) is not an investment. It is a tax shelter. I told students to think of them as a magic box covered with IRS repellent (here, let me highlight my non-existent artistic talent).

While the investment is in the tax shelter, any investment income earned is free from taxes. In other words, it is yours to keep and will compound tax-free (which can be a big advantage). The reason it is a big advantage is that investment income is generally taxed. Short-term capital gains (investment profits on investments held less than 1-year) and interest income are taxed as ordinary income. Long-term capital gains and (most) dividends are taxed at favorable rates, but still often at non-zero tax rates. This means that if you bought a stock at $60 and 6-months later were lucky enough to sell it for $100, you “made” $40 in capital gains. However, if you are in the 22% tax bracket (an individual with $50,000 in taxable income would fall in this category), you really only earned $31.20. Not bad, but not $40. Another way to look at it is your 67% return ($40/$60), just became a 52% return ($31.20/$60).

Since the tax shelter’s return is generated by the investments, then your return will depend on what you put IN the tax repellent box. If you put in lower-risk investments (Bank CDs, Treasury Bonds, high grade corporate bonds, etc.), you will probably earn relatively safe, but low, average returns. If you put in higher-risk investments (stock-based mutual funds, Real Estate Investment Trusts, etc.), you are likely to have more volatile, but higher, average returns. You could also put individual stocks in your tax shelter and, assuming it is a small, relatively undiversified portfolio, you will have even more volatile, and not necessarily higher (or lower) returns.6 IRAs allow you more flexibility to put in individual shares (or, in Peter Theil’s case, even founder shares). 401(k) and 403(b) plans are going to be more diversified portfolios (mutual funds).

Another question that came up a lot in classes was whether a traditional or Roth version was better. One of the more common answers in life applies here — it depends. First, you need to consider eligibility for the up-front tax deduction on the traditional (this is not an issue for the employer-sponsored 401(k)/403(b) versions or for an IRA if your employer does not offer a pension plan). In 2021, if you are single and make more than $66,000 in adjusted gross income, you can no longer make the full contribution and at $76,000 you can no longer participate. These numbers jump to $105,000 and $125,000 if you’re married. The Roth IRAs offer a little more flexibility, as the participation limits jump to $125,000/$140,000 for a single person and $198,000/$208,000 for married couples.7 Therefore, if you make too much for a traditional IRA, the Roth is a better option (unless you make too much for that as well). A second issue has to do with how much you plan to have in your retirement account as that will impact the tax rates you face in retirement. The more wealth you accumulate in retirement assets, the greater your income in retirement (which leads to higher marginal tax rates). In other words, if you are going to get to retirement with a relatively small amount ($300,000 or less), your retirement income will probably be low enough that the back-loaded tax benefit of the Roth is less attractive. Alternatively, if you are going to have $2,000,000+ in your retirement funds, your income in retirement will likely be high enough that the back-loaded tax benefits become more significant.

The IRA vs 401(k)/403(b) issue also comes up. As a general rule, take your free money if your employer offers you a match. Contribute up to the match amount first. Remember in our example from the TL;DR summary that the employer match added about $350,000 to our wealth. That’s not nothing! After that, it depends on your preferences and the investment choices in the employer’s plan. If you love managing your own portfolio, you might want to stop contributing to the employer’s plan as soon as you meet the match level and switch to an IRA. Also, if your employer’s plan has limited choices or high expense funds, you may be better off by switching to an IRA after getting the maximum match. In most cases though, there will not be a significant difference and the bigger factor will just be making regular contributions over time.

The assumption of a 13% tax rate on investment income is due to the varying tax rates on short-term vs. long-term capital gains, interest, dividend and how often an investor trades. This also does not take into account any pay increases over your career. The 37 years would take someone from 25 years old to 62 years old. Think of this as an approximation as several assumptions need to be made.

The employer is still related to the IRA process in that donations need to come from “earned income” which means a salary or hourly wage. You can not use dividends, interest, capital gains, etc. to fund the contribution.

A lot of good info on IRAs can be found in Traditional and Roth Individual Retirement Accounts (IRAs): A Primer. There are also Rollover IRAs (to transfer your 401(k)/403(b) plan to after you leave your employer if you’d like) and SEP IRAs that can be used as tax shelters.

The non-working spouse contribution was almost a bad joke until 1998. A non-working spouse could contribute a maximum of $250 per year. Assuming that was put in at the beginning of each year for 40 years and the account earned 10% per year, that would grow to just under $122,000. While that is nothing to sneeze at, I’m guessing the number of people who would have done this is well under 1% of the population and it would still only generate about $9000 per year in retirement (assuming a 25-year retirement with 6% returns) if by some <sarcasm>one in a million event occurred that resulted in the couple splitting up were to occur.</sarcasm> Fortunately, in 1998 it jumped to a more reasonable $2000 for a non-working spouse.

401(k) and 403(b) plans can be set up as traditional or Roth versions as well.

Note that I say “likely” here. That is because the nature of risk deals with expected returns (what we can expect to earn on average if we repeat the holding period an infinite number of times). I’m not sure about you, but I’ve never been able to replicate a holding period more than once. This means that my actual return is likely to end up higher or lower than my realized return. The greater the level of risk, the less reliable that expected return is.

These income guidelines typically go up by a small amount each year.