Happy Thanksgiving!

A Short Post for the Holidays

Since it is the week of Thanksgiving, I’m going to try to keep this week’s post on the shorter side so everyone has time to enjoy family, friends, turkey (or ham…we’re skipping the turkey this year), cranberries, pies, football, and pies. Yes, I said pies twice, because if you aren’t having multiple servings of pie, you are doing this week VERY, VERY wrong! The picture below just needs a bit of whip cream.

The theme of this week’s post is going to be just a few brief thoughts. So let’s get started.

Thought #1 — Curating Your Social Media

One of the recurring questions of the past several years is how much damage social media is doing to society? The answer, as almost always is the case, is “it depends”. Social media can be a great tool to keep in touch with people who are outside of your immediate geographic area and develop interest networks. I talked about this awhile back when reviewing Liberty’s Highlights — social media allows us to connect with people who share similar interests. This can be damaging (too much time in a social bubble may make you think that everyone shares your views) or highly beneficial. Which one depends on you.

I’ve mentioned before that I like to run. One of the main places I hang out in Facebook is a running group of a small set of friends, most of whom I’ve never met.1 To be honest, I may no longer be running if it wasn’t for the group. It creates a bit of peer pressure during those lulls when I’d rather hang out on the couch for a week instead of run. However, I know exercise is important for both my physical AND mental health, so I appreciate the group not only for their friendship, but also for keeping me active. If you have the proverbial crazy aunt/uncle who spends their day posting conspiracy memes which drives your blood pressure up, remember — YOU control YOUR feed. Unfollow people who don’t add value (and value is not always happiness, but it is stuff that sparks an interest and raises your curiosity about things which YOU find interesting and engaging).

Whether it is FinTwit (at least some of FinTwit), fantasy sports, hiking, or running for me or whatever it is that strikes your fancy for you, follow it. Whenever someone posts stuff that is looking to create division, reach for the unfollow button. If you’ve emailed me, you’ve seen my sig line. The addition by me is essential...life is way too short to spend it getting aggravated.

"Twenty years from now you will be more disappointed by the things that you didn't do than by the ones you did do. So throw off the bowlines. Sail away from the safe harbor. Catch the trade winds in your sails. Explore. Dream. Discover." -- (allegedly) Mark Twain

"Twenty years goes by quicker than you'd think." -- Me

Thought #2 — Tax Time Approaches!

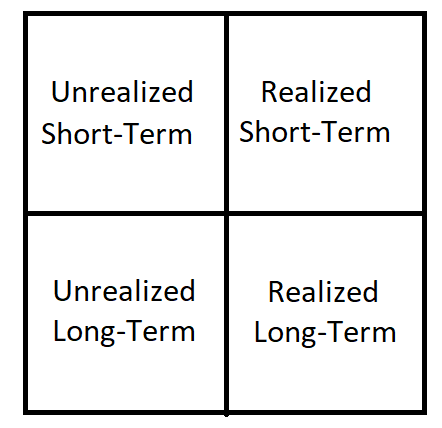

One of the themes of my posts is to focus on after-tax returns.2 If your investments are in a tax sheltered account such as an IRA or 401k, you can skip this thought. However, if you have money in a taxable account, now is the time to think briefly about managing the capital gains tax implications on your portfolio. Remember that capital gains are split into a two-by-two matrix.

For the holding period, the cutoff point is one year. If you have owned the investment for one year or less, it is a short-term capital gain and will get taxed as ordinary income. On the other hand, if you’ve owned it for more than a year, it is a long-term capital gain and will receive more favorable tax status. If you are married and filing jointly with taxable income of $120,000, your long-term capital gains tax rate is 15% while your short-term capital gains tax would be 22%. While that isn’t a huge difference, it turns an 8% pre-tax return into either a 6.8% or a 6.24% return. Enough of a difference that it is probably worth monitoring to some extent.

For realized vs. unrealized, the difference depends on whether or not you’ve sold the security. If you have, it becomes a realized capital gain (or loss) and impacts your taxes. If you haven’t sold it yet, it is not relevant in the current tax year and won’t be until you sell it. So lets take a quick look at the rules:

Unrealized capital gains don’t matter, so don’t worry about them. If you don’t sell a position, it’s not relevant.

If you do sell a position, remember that capital losses offset capital gains in the current year. Therefore, if you sold a position this year with a $10,000 gain and didn’t offset that with a capital loss, you owe taxes on the full $10,000. However, if you have a position with a $6000 capital loss, that lowers your taxable capital gain to $4000.

Your maximum capital loss for the year is $3000. After that, you can carry forward capital losses indefinitely. However, you can not apply them retroactively.

This implies that if you sold stocks with a capital gain this year, you ideally want to look for positions with capital losses to offset those gains without going beyond a $3000 net capital loss. While you can go beyond $3000, there is no current advantage and it gets carried forward to next year.

One other important concept is the “wash sale rule” which says that if you sell a stock today, you can not rebuy a “substantially similar” stock within the next 30 days and still claim the capital loss in the current year. In other words, if I sell 100 shares of Ford for a loss, I can’t turn around and buy back 100 shares of Ford the next week and still record the capital loss. I have to wait a month to buy it back in order to do so. However, I could sell shares of Ford and buy shares of General Motors and be fine while still retaining exposure to automotive. I would not be exposed to Ford company-specific issues.

If you haven’t done so, now is the time to look over your taxable portfolio to see if there are any tax-specific transactions you want to make.3 One cautionary note is to be careful not to focus purely on taxes. If it is a position you want to maintain, don’t sell it purely for the tax harvesting factor or it may move before your 30 days is up.

Thought 3 — Be Grateful

As I mentioned at the top of the post, this is Thanksgiving week. One of the themes of the holiday is something that should not be limited to Thanksgiving, but ideally would become a standard part of our lives — be thankful/grateful for all the good fortune that falls our way. This is one of those themes that I think is too important not to be repeated, but we all have headwinds (forces that impede our progress) and tailwinds (forces that accelerate our progress) in our lives. Human nature is to give ourselves credit for the tailwinds and blame others for the headwinds…and there is likely some truth to that. However, it is only some of the truth. While we can influence our life’s outcomes, we do not control those outcomes. It is a subtle, but important difference. Shift away from negativity and focus on being grateful for the tailwinds at your back and the headwinds that you’ve either dodged (which is difficult because we are often not even aware of them) or overcome. Celebrate Thanksgiving by being thankful and keep that mindset throughout the year!

So, without further delay, get out of here and enjoy the holiday with you family and friends. Also, and this is essential, the one on the LEFT is the correct choice. Don’t let anyone tell you otherwise!

HAPPY THANKSGIVING EVERYONE!

There are technically 56 “members” of the group, but I’m guessing the active membership is probably closer to 15 who post semi-regularly in a “daily” thread. I’ve run with 4 different members of the group and that is over about a 7-8 year window.

Disclaimer — this is a discussion of taxes in theory and not specific tax advice. Always check with a tax consultant or do your own due diligence before making any trades based on tax issues!

Full disclosure. I sold my position in Dollar Tree on the runup after their earnings report. It was a great short-term investment that I was hoping would be a longer-term investment, but given that I was up over 60% in a few months, I decided to cash out. To complement that decision, I also liquidated two positions that I had a loss on in order to offset some of the capital gains. Hopefully that won’t come back to bite me over the next month.

Happy thanksgiving Dr. Bracker!