Gladstone Land Corp -- Risks Part One

Risks of the Business

Disclaimer — This is an informational process and is not designed to tell you whether or not you should buy Gladstone Land Corporation (LAND 0.00%↑). Instead, it is designed to show you how I would go about the evaluation and what questions I have. DO NOT USE THIS SERIES TO MAKE A BUY/SELL DECISION!

Note that this is a different, multiple part (maybe too much) attempt to look closely at a company. Please let me know what you think and feel free to offer suggestions for improvement.

Risks Associated with Gladstone Land Corp

The next 11 pages deal with various business risks associated with investing in Gladstone Land. While, many of these are going to be “boilerplate” we are going to go through each one in varying degrees of detail.

These are the first three risks documented in the 10K. Yes, I know there are more, and don’t worry, we’ll cover them all (even one’s where you’re wondering why would they even put that in there) in this week’s update.

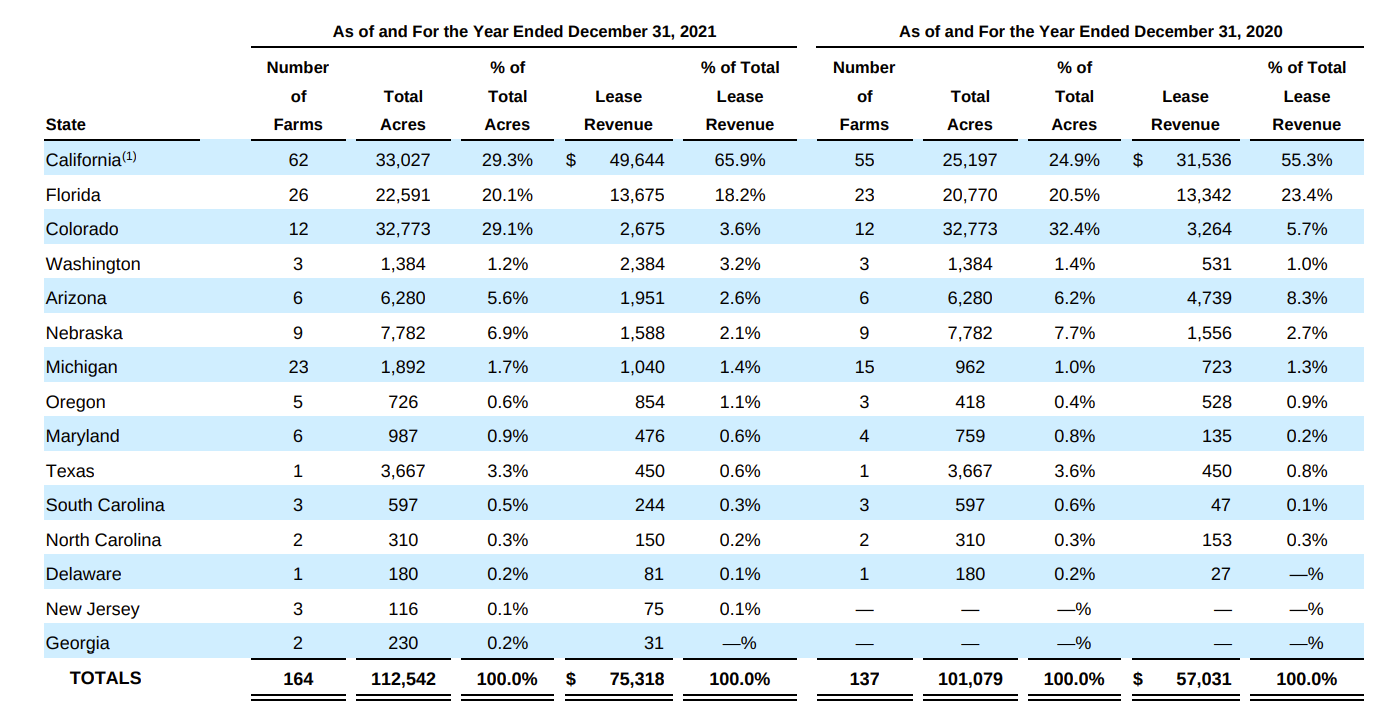

The first risk is geographic. While there are 50 states in the US (plus Washington, DC and some territories), Gladstone currently has property in only 15 of the states. You can see the states here (and bonus points — figuratively — if you can name each of them).

These states have different weather (a drought in California could be offset by a freeze in Florida), legislations rules regarding real estate are slightly different in each state, regulations on taxes are different, etc. Here is a breakdown of their geographic representation. As you can see, California and Florida are their biggest (by far) arenas representing 84.1% of their lease revenues. There are a lot of differentiation in types of crops, but overall your leases are tied to two states, which is going to increase the risk exposure.

Their second concern is that there may not be ample opportunities. This is probably more relevant as more commercial farmers are competing for farmland. In addition to Gladstone Land, you have AcreTrader (I do own farms through them) and many other private farmland investors.1 The more commercial enterprises competing for farmland implies far fewer viable investment opportunities for growth. Make sure you understand that tradeoff…this is not a get rich quick opportunity.

The third concern has to do with permanent crops that need developed. I invested in two of these in my AcreTrader account where they anticipate it will be a couple of years before cash flows are being generated. One is an apple farm where the investment closed at the end of March 2021 and the first (limited) harvest is not until 2025 (which will be limited) and the first full harvest is not expected until 2027. That means it will be 7 years before the first real returns kick in. A lot can happen to apple production, pricing, etc. in 7 years! This makes a higher risk investment. Fortunately, this appears to be more of a “cautionary” risk as the following line is in the 10K (emphasis added by me). Not to be dismissed (as it could happen), but not a current risk factor either.

All of our properties undergoing development or planted with immature permanent crops are currently leased and earning income. However, with regard to future acquisitions of such properties, the time frame required for development and for the farms to become commercially productive means that we may not be able to lease the farms and, in turn, generate revenue with respect to such farms for several years.

Here are the next set of risks mentioned in the risk category.

The fourth risk mentioned here is technically valid as no one knows what the future will bring. That said, their Q1 Conference Call states

Our farms continue to be 100% occupied and are leased to 86 different tenant farmers, all of whom are unrelated to us. And the tenants on these farms are growing over 60 different types of crops. Given the number of different growing regions, tenants and different tenants and different types of crops on our farms, we think there -- this is sufficient diversification to provide safety and security for the cash flows coming in from the rents. We believe these diversifications help protect the dividends that we pay to our shareholders.

There is also this line from a paragraph or two later

The tenant there wanted to see how it worked before he signed a long-term fixed rate lease. So we're going to get 80% of the gross revenue earned on the farm this year based on current commodity prices and yield estimates, we think we'll end up in a similar place, where we would have been in -- on the previous lease on this farm, but we will not know the results until the end of the year when the crops are sold. Excluding this one lease, our other lease renewals are expected to result in an increase in annual net operating income of approximately $55,000 or about a 3% increase over the old leases that we replaced.

These exchanges indicate that there are some potential lease issues that could arise. However, at the moment, they appear pretty small.

Regarding the cash dividends, it is important to note that their latest conference call includes the following

Finally, regarding our common distributions. We recently raised our common dividend again to $0.0454 per share per month. Over the past 29 quarters, we raised our common dividend 26x resulting in an overall increase of more than 51% over this time. Since 2013, we paid 111 consecutive monthly dividends to common shareholders, and our goal is to continue to increase the dividend at regular intervals.

and this

On a quarter-over-quarter basis, adjusted FFO for the first quarter was approximately $6.4 million compared to $6.7 million in the fourth quarter last year. And AFFO per share was $0.185 in the first quarter versus $0.199 in the fourth quarter '21. Dividends declared per share were about $0.136 in both quarters.

This indicates that while, again the future is unknown, the ability to pay dividends is not a major concern at the moment.2 While bankruptcy is a minor potential concern, it is more of a temporary issue (and one that Gladstone Land has yet to face) as their properties are such that a new tenant could be found without much difficulty.

Our next set of risks are here.

The first is a risk, but also an opportunity. Given higher inflation (especially in food), shorter-term leases can be as much a potential gain as a loss. If I purchased a piece of farmland and leased it out in January 2020 or leased it out in March 2022, I’m expecting that I’d get a much better deal on the lease in March 2022 than I would’ve in January 2020. Charlie Munger is famous for his “Invert, always invert” quote. Risk is one of those situations as well. The flip side though is we need to think not just about what is happening now, but what will happen over time (what if lease rates decline?).

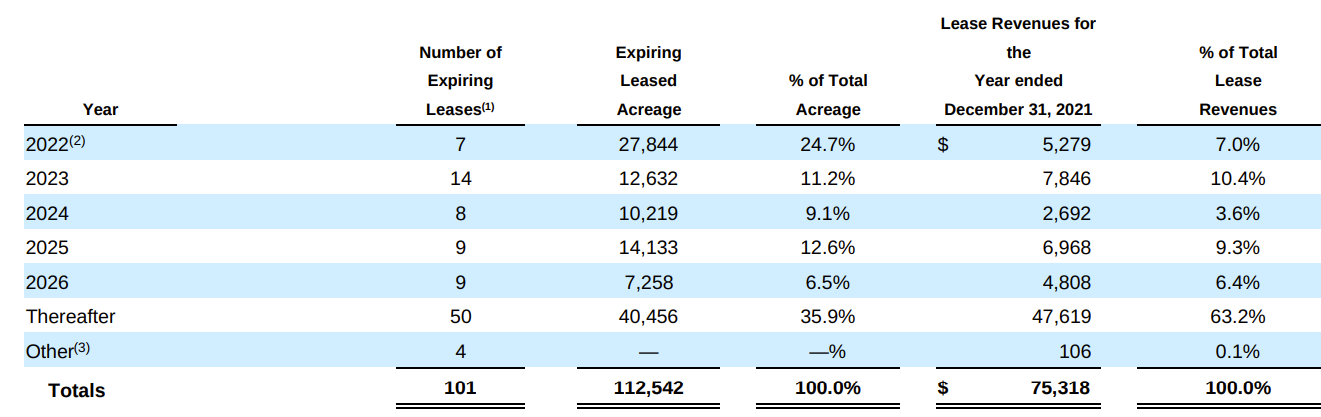

The next risk is just a longer-term outlook on the previous. While some risks are short-term in nature, the opposite is a longer-term lease of 5+ years. Again, this is mitigated to an extent by rental rate escalations, but these are typically fixed in the contract. This is likely part of what has led to a decline in LAND’s prices over the past 6-months as property rental rates are rising slower than the value of the land itself. Fortunately, Gladstone Land owns the farms, so ultimately it is more of a short-term problem rather than a long-term problem.

While participation rents are a potential issue, these account for only about 25% of the farms (39) and about 30% of the farmland (34,477 acres).3 Therefore, it is probably not a major concern.

The last risk factor is probably one of the more relevant risks (and again, an opportunity). Permanent crops are higher risk, which means higher expected returns. If there is a problem with the crops (weather, disease, etc.) it is going to be more costly. There is also a more permanent nature of the plants (you can’t decide to replace your almond orchard with apple trees from one year to the next) which increases risk. How much risk vs. return are you interested in taking on?

The next set of risks are a mix of boilerplate with some real issues as well.

The first and second risks mentioned here are what are typically referred to as boilerplate. Yes, they are real risks, but they account for a very minor portion of the risk in Gladstone Land. It may be difficult to sell or re-lease property, but it is nowhere near an impossibility. You can see here that Gladstone Land has staggered lease termination (these are official, not an early termination which would be far more rare) to reduce the issue.

The one that is a bigger potential risk (especially given increases in drought conditions) is the potential lack of water. Granted, Gladstone Land looks at this as a major factor in acquiring land (see last update), but things do change. One way that Gladstone is addressing this is with the purchase of banked water resources at some of their properties.

During the year ended December 31, 2021, we executed all three contracts to purchase all 45,000 acre-feet of banked water for an aggregate additional cost of approximately $ 2.8 million.

This does not mean lack of water is going to disappear, but it appears that it is being addressed adequately.

The weather conditions issue has already been addressed. However, insurance does provide some protection (although prices may increase with poorer weather conditions going forward).

The climate change issue is a bigger problem. Unless you’ve been living in a cave for the past 20 years, you’ve heard about climate change. While it is not a universally agreed position it is hard to argue that regardless of whether this is a temporary fluctuation or a more permanent change, temperatures have been rising, oceans are warming, and ice sheets are melting, and snow cover is declining. Maybe this reverses and maybe it doesn’t.4 That said, climate issues are changing public behavior which will carry over to farming. This is an important risk that Gladstone Land will be facing, but again, it is also an opportunity for them. The question becomes how they will attempt to manage the risk. Will they overreact or underreact to potential changes?

Getting tired of risks yet? Don’t worry, we’re about halfway done. 🤣

These are all primarily focusing on the same aspect — the impact of financing availability through additional equity or debt (leverage). One important aspect of REITs is that they must pay out about 90% of their income each period in the form of dividends. This means that they are going to have very little in the manner of retained earnings to fund expansion. However, Gladstone Lands is expanding. So where are they getting the money to do so?

The first risk address the need to raise capital through equity (Series B preferred, Series C preferred, Series D term preferred) or raising debt in order to continue to fund growth. This is normally not a major problem, but could run into issues if the funding becomes more difficult. The second risk refers to the possibility of leverage (increasing debt obligations) which opens them to the same constraint. Currently, their debt costs are as follows

the weighted-average term to maturity of our notes and bonds payable was 9.8 years, and the weighted-average remaining fixed-price term of our borrowings was 5.6 years, with an expected weighted-average effective interest rate of 3.36% over that term.

It may be a bit higher now given rising interest rates, but probably not significantly.

The next three risk factors are not likely to be real important. Yes, they could have a bad year and need to cut dividends, but again that hasn’t happened in the recent past. Remember the dividend policy:

The Company has paid 110 consecutive monthly cash distributions on its common stock since its initial public offering in January 2013 and has increased its common stock distributions 26 times over the prior 29 quarters.

As for too much leverage, that is one of the points of the business is that they should not overextend themselves. History has shown that this isn’t a major problem so far. Finally, they express concern that too much debt financing could cause problems for them. Again, technically a potential concern, but nothing has raised this fear at the moment and the weighted average effective cost of debt being at 3.36% indicates it is not likely to be going forward.

Next set of risks

The first of these just stresses that the liabilities on some of their properties are connected. In other words, a mortgage on property A may also contain a mortgage on property B. This is unlikely to be an issue as long as the advisory team adequately manages their debt.

The next set just talks about competition for land. As we’ve established, this is not a situation where Gladstone Land is going to be acquiring farmland and earning 25% annual returns. Farmland is pretty well scrutinized and they are likely to earn between 6-10% returns split between rent and return on land.

We’ve covered dividends before, so I’m not going into this one again. Also, failure to succeed in new markets is an issue that virtually every company faces. We’ll chalk these two up as immaterial risks.

The last issue deserves a bit more scrutiny. Essentially they are talking about the prospects of land that gets transitioned to an urban or suburban use due to land expansion. They state in the 10K that (italics added)

Although the current development market contains uncertainties, these uncertainties may be more acute over time, since we do not intend to acquire properties that are expected to be converted to urban or suburban uses in the near term. As a result, there can be no guarantee that increased development will actually occur and that we will be able to sell any of the properties that we own or acquire in the future for such conversion. Our inability to sell these properties in the future at an appreciated value for conversion to urban or suburban uses could result in a reduced return on your investment.

So, while this is a potential issue IF they were acquiring property with plans to move it from farmland to say an apartment complex, they are not acquiring properties that are expected to be impacted at the moment. Probably not a significant concern.

Yes, there are more risks. The good news is we’re almost done with the risks to the actual business…then there are one’s about the risks from using an advisor, risks associated with REIT structure, and risks about different share types. I’m going to hold off on these for a bit. You’re welcome!

Honestly, we’re going to speed through these risks as most of them are not really that surprising. The first has to do with insurance coverage. Some conditions (war, weather-related disasters, etc.) are going to create issues. Also, some insurance plans will require deductible payments, etc. Hopefully this is greatly reduced by the range of farms that Gladstone Lands is operating.

There is potential liability for environmental damages. Again, this should be greatly reduced by the advisory service, geographic diversity, and legal protection within the lease. Specifically, the 10K states

We will generally include provisions in our leases making tenants responsible for all environmental liabilities and for compliance with environmental regulations, and we will seek to require tenants to reimburse us for damages or costs for which we have been found liable. However, these provisions will not eliminate our statutory liability or preclude third-party claims against us. Even if we were to have a legal claim against a tenant to enable us to recover any amounts we are required to pay, there are no assurances that we would be able to collect any money from the tenant.

The inability of tenants to follow labor regulations is a potential issue. Again, the number of farms makes this less of an issue, but there is the possibility of minimum wage issues and illegal immigration which are higher in farming occupations than other areas.

I’m not going to get into the presence of engangered species as that seems like a minor issue and, again, limited by the geographic spread of farms. The same is true for mineral rights issues.

This leaves interest rate risk. I’m not sure, but I’m guessing just about every company has this listed in their 10K as a potential concern because (a) interest rates fluctuate and (b) interest rate fluctuations can cause problems. This is true for almost every firm that has leverage (debt) either directly or through leases. It is also true for almost every firm that relies on customers who would also be affected by leverage (debt). Is it a real risk? Sure. Is it a relevant risk tied specifically to Gladstone Land? No.

What’s this? The final set of business risks? YES!

The first of these risks is one that has already been addressed, albeit in a slightly different format. Gladstone states

These increases in the federal funds rate and any future increases due to other key economic indicators, such as the unemployment rate or inflation, may cause interest rates and borrowing costs to rise, which may negatively impact our ability to access the debt markets on favorable terms and the market value of our capital stock.

Essentially, no one knows what the future action of the Federal Reserve and other regulatory bodies will be going forward.

Cybersecurity risks are a relatively recent addition to many 10Ks, but they are relevant. Company spending on mitigating information security has increased over the years and this will likely not disappear.

We have implemented or plan on implementing additional processes, procedures, and internal controls to help prevent, detect, and mitigate cybersecurity risks and cyber intrusions, but these measures, as well as our increased awareness of the nature and extent of a risk of a cyber-incident, do not guarantee that a cyber-incident will not occur…

The last risk is definitely a newer one as in 2019, COVID was non-existant. That said, it is now which has caused many firms to recognize and respond to the risk of COVID and other public health emergencies. As a grower of produce, Gladstone Lands is going to feel the impact on shipping, shortages, etc. of any shutdowns and thus, it is likely to introduce some instability. That said, COVID (and other potential health situations) are impacting all businesses (hello, Peloton!).

Of the 37 different business risks, the three that I think are the biggest challenges for Gladstone Lands would be

Geographic Diversity — While there is a lot of the country that has farms, current regulations restrict investments by companies like Gladstone Land (specifically, Iowa, North Dakota, South Dakota, Minnesota, Oklahoma, Wisconsin, Missouri, and Kansas) in their states. This means that while Gladstone does have 15 states that they have farms in, 84.1% of their leases (as of the 10K) were in California and Florida. Granted, there is crop diversity across these ownership structures and some geographic dispersion, it is probably less diversified than we’d like.

Potential for Additional Growth — Farms are not exactly a “growth” business. Instead, there is a strong tendency for more yield to be produced on fewer acres of land. There are also a lot of institutions looking for opportunities. The more people looking for opportunities, the fewer you would expect to find. The reason to invest in Gladstone is partly a diversification story (farmland behaves differently than other businesses), but it is no different than tech vs. retail vs. financial. Gladstone is not creating new farms. They are owning the land and using it to create shorter-term (typically 3-10 year) leases and profiting from the rental rate plus land appreciation.

Climate Change — One of the bigger risks for Gladstone is the potential climate change issue. As we see less water, warmer temps, less snow formation in winter, etc., this will be an issue that will require Gladstone to focus on getting the best production from the environment. Fortunately, people need to eat and farms are essential in that process. While this may require more attention, it is a risk that could represent an opportunity for Gladstone if managed correctly.

Did you know who the largest owner of farmland in the US is? Bill Gates (Former Microsoft Founder). “Along with his wife Melinda Gates, Bill owns over 268,000 acres of farmland diversified in over 19 states. Gate's private American farmlands are worth an estimated $690 million.” That’s over twice Gladstone’s 112,542 acres. The information may be a bit dated as it is referring to his wife Melinda who he divorced in May 2021.

Adjusted Funds From Operations is a REIT term that gets away from GAAP (as it should) because real estate is very different than most businesses. You can see an explanation here.

This is reported on the top of p. 45 of the 10K.

I’m in the camp that climate change is real but can be addressed with positive choices regarding technology. My confidence on this prediction is relatively weak as (surprise) I’m not a climatologist.