Gladstone Land Corp (LAND)

Overview of the Firm -- 10K Part One

Disclaimer — This is an informational process and is not designed to tell you whether or not you should buy Gladstone Land Corporation (LAND 0.00%↑). Instead, it is designed to show you how I would go about the evaluation and what questions I have. DO NOT USE THIS SERIES TO MAKE A BUY/SELL DECISION!

Information Gathering — Start With the 10K

Okay, we’re going to start covering Gladstone Land Corporation. One thing you’re going to want is the firm’s most recent 10K (use the link to download), as that is where we are going to start. Note that there is a lot of extra information in the 10K, so my plan is to go through the pages and highlight things that I think are important. We’re going to start by assuming you know almost nothing about Gladstone Land.

The first thing we need to do is identify what the business does and how it plans to make money.

This is on page 6 of the 10K and provides an overview of how the company intends to make money. The ability to generate free cash flows is always important for every company as the value of the stock should be equal to the present value of all the free cash flows it is going to generate into the future. Granted, this is a moving target as those cash flows have not occurred yet. Therefore, it is really equal to the market consensus of the expected cash flows and the discount rate…neither of which we know.

However, our job is to estimate them to the best of our ability and then monitor the firm’s progress in their ability to reach them, exceed them, or not meet them.

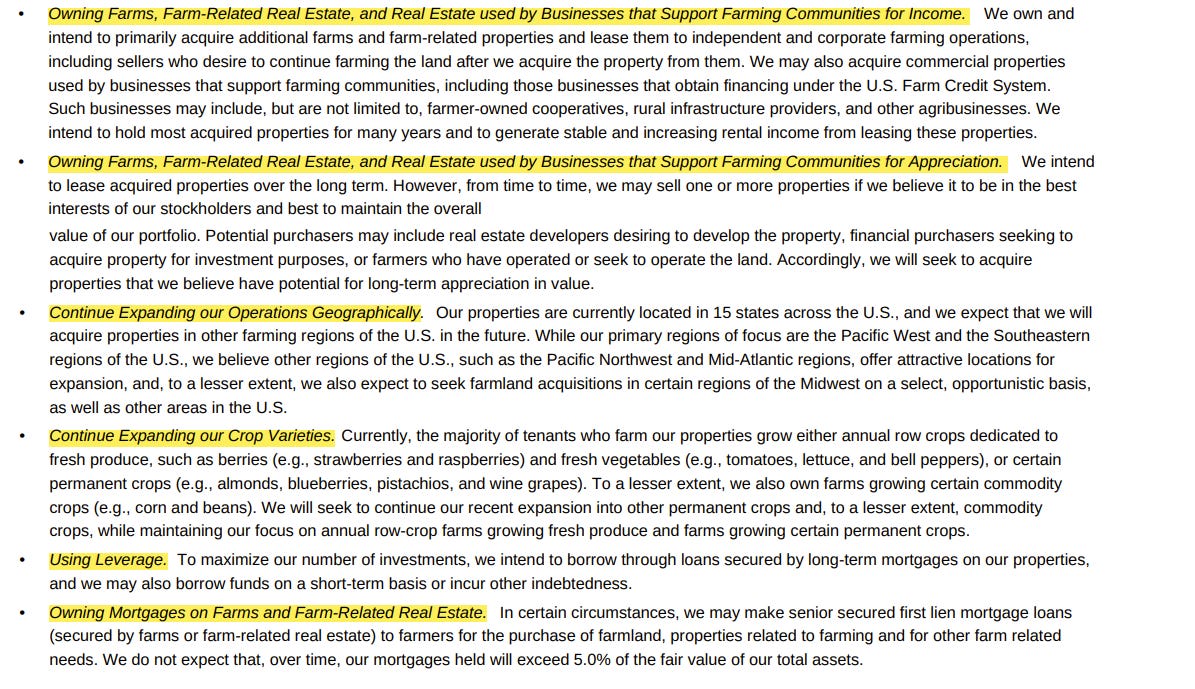

We note that their business is to own farms (164 farms comprised of 112,542 acres across 15 states) and other farm-related resources.1 Their focus is on farms that produce annual row crops (such as strawberries) or permanent crops (such as almonds). However, they also own some commodity crops (corn/beans) and farm-related facilities (cooling, processing, etc.). They intend to continue to do this going forward (acquiring new land).

The next question is how do they intend to make money off of this land and facility ownership?

They plan to do this through a three-pronged approach:

Distributing dividends

Appreciation of land/facility property

Capital gains when selling their land

Note that this is essentially a case of planning to earn money on the property (rents) and have the property increase in value over time. They want to focus on the following factors to achieve their goal.

Owning farms/farm-related real estate for income

Owning farms/farm-related real estate for capital appreciation

Expanding operations geographically

Expanding crop varieties

Using leverage

Owning a small percent (less than 5%) of the total assets as mortgages

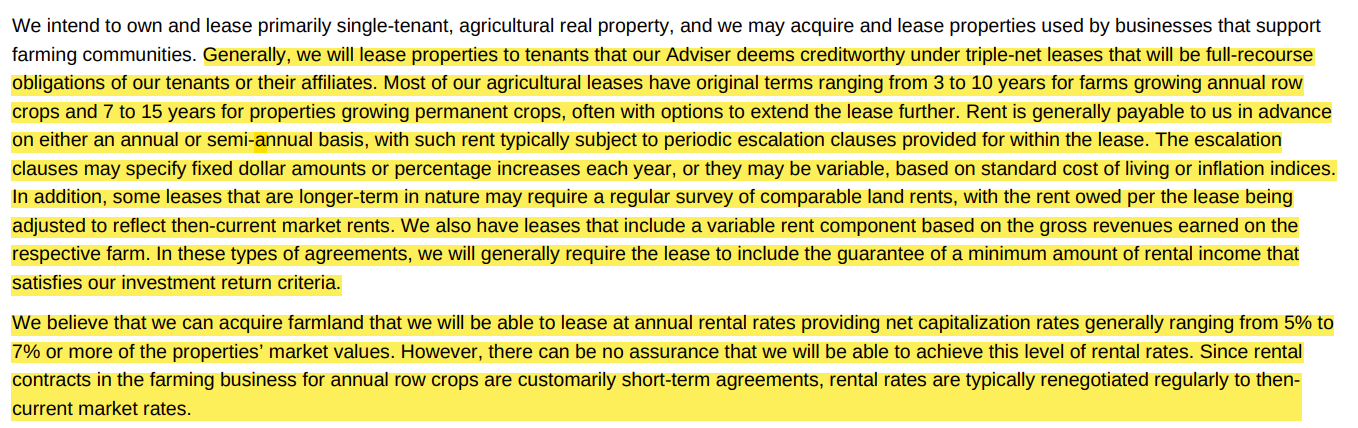

Let’s take a moment here to discuss the “triple-net” lease structure. There are three basic leasing structures. A single-net lease implies that the tenant/lessee pay property tax in addition to the lease payment. A double-net lease implies that the tenant pay property tax and property insurance. The triple-net implies that the tenant is responsible for all payments including maintenance of the property. Granted, that is not their only lease format, but their primary leasing format. Essentially, it means that the tenant makes a fixed payment for the property over a set time frame and is responsible for maintenance that is not specified in the lease contract. The risk is that at the end of the time frame, Gladstone is responsible for renewing the tenant or finding a new one.

So, most of their leases are triple-net, full-recourse obligations of the tenants which means they are likely to be paid off. The average obligation for farms growing annual crops is 3-10 years, while those growing properties with permanent crops are 7-15 years. Since Gladstone is leasing the property on a triple-net basis, there is little risk of default (low-risk) which also is going to imply a lower return. The properties allow for rates to change (typically increasing) by a fixed dollar/percentage amount or they may be subject to cost-of-living adjustments. Some leases will adjust rental rates based on current market rates or include a bonus payment if the yield/price is high enough. This last type of loan is beneficial to the farmer in that it may reduce the benefit of a big year, but also reduces the risk (as the base price is usually a bit lower).

The net capitalization rate refers to the net operating income from the lease divided by the market value. This is expected to be in the 5-7% range, but may be a bit lower or higher if there is market volatility.

When looking to select land for the REIT, what types of things are they looking for?

Water Availability — This is obviously a major concern in many areas as there are water-intensive crops in places with relatively limited amounts of water (see images of water declines at Lake Mead). Without water, farms are going to be less productive (or with too much water).

Soil Composition — I did not realize how many types of soil make up most fields until starting to buy a couple properties with AcreTrader. It’s a lot! Soil composition must match the type of field that the crop is being grown on.

Location — What is the phrase in real estate? Location, location, and location! Farming is going to need to be set up in the right location for both growth and harvesting.

Price — In most business decisions, this is going to be a narrow range which makes both the lessee and leasor happy. One thing to consider is economic expansion. The closer the property is to an urban environment, the more likely the town will grow out to the property. This has potential upside, but also is going to make the property more expensive to acquire.

Granted, these same four factors are what everyone is looking for in acquiring properties. It’s not exactly like Gladstone Land found the secret formula and decided that water, soil, location, and price were going to make them rich. So, really we are trying to figure out if the Gladstone Land advisors are competent. The advantage is this is not a “Get Rich Quick” scheme. Instead it is a lower risk, lower expected return scheme that should generate, on average, low positive returns over time that match (less expenses) the returns of owning farmland.

The above deals with the land that they are acquiring. Next, we want to look at the tenants that they seek to rent the land. Remember, the tenants do not own the land, and instead are renting it (on a multi-year basis). Therefore, the risk for Gladstone Land is are their tenants going to be able to reliably pay the rent. Also, note that not all of these are requirements.

While I’m not going to go through each item, I do want to address one that will show up again. Diversification is important in that they want to be a farming REIT that will allow investors to own not a single property or a single type of farmland, but a diversified portfolio of farmland. Things like strawberries, blueberries, wine grapes, almonds, pistachios, etc. While each market may have individual gyrations, it is unlikely that food as a whole will lose value. Thus, they want to spread out both their locations (15 different states — we’re going to come back to this in the next episode on business risks, but over 80% of lease revenues come from California and Florida) and crops to provide a bit of a cushion. It is still farmland, but not the same type of farmland.

Another key piece of their operating structure is how much debt is going to be used to finance their investments. If no debt is employed, you are simply going to earn the value of the farmland less expenses. On the other hand, effective use of leverage means that, for example, if I borrow money at 3% and invest it to earn 5%, I’m getting a “free” 2% return.

Granted, it is not truly free as it creates an obligation that must be paid by me for a variable return — I “think” I can get 5%, but I “know” I have to pay 3%. If the 5% fails to materialize, I’m going to lose money. Therefore, leverage should be used in a limited fashion2. This also allows the firm to acquire more property because they have the borrowed money plus the investors equity to invest. So, their job is to balance the potential benefits (higher returns and more property ownership) against the cost of the higher risk (debt obligations need to be paid on time).

There are also multiple limitations that Gladstone Land makes on the property it chooses to invest in.

One cautionary note is that Gladstone Land is not separated from it’s other types of businesses. Specifically, Gladstone runs four different REIT/companies as follows:

This implies that there is the potential for agency risk. David Gladstone is in charge of GLAD, GOOD, and LAND. It is important to make sure that the ownership of the company is not doing anything to enrich itself or his family.3 Depending on how comfortable you are with the various conditions on LAND’s ability to “control” the behavior of the CEO, this is going to be an essential issue to think about.

It is something that I am “okay” with. By “okay”, I mean that I would prefer it if the person in charge of Gladstone Land Corp was just running Gladstone Land without the other businesses. It is not a simple task to run multiple companies (even with overlapping lines of business). That said, it is not a deal-breaker in and of itself, but does raise an eyebrow to watch over. Reading about the implementation put into place is different than being there to see how it is implemented. This DOES make me a little nervous.

One way to check on this is to look at Yahoo!Finance’s Corporate Governance Score which js not exactly “on board” with Gladstone’s arrangement. This is an area that raises a bit of concern.

Gladstone Land Corporation’s ISS Governance QualityScore as of July 1, 2022 is 8. The pillar scores are Audit: 6; Board: 10; Shareholder Rights: 9; Compensation: 4.

Corporate governance scores courtesy of Institutional Shareholder Services (ISS). Scores indicate decile rank relative to index or region. A decile score of 1 indicates lower governance risk, while a 10 indicates higher governance risk.

As you can see high scores indicate higher governance risk (not lower). Seeing the Board given a 10 and Shareholder Rights a 9 does not inspire confidence.

This wraps up our introduction of what Gladstone Land Corporation is and how it intends to make money (what strategies are they following). It also address the agency risk inherent in the format. I like the business as a way to own farmland. It also focuses more on permanent crops than traditional corn/soybean type farms which is a plus. The diversification across geographic arenas and crop types are both benefits. Note that the goal here is not to identify the “best” land, but instead to have access to farmland as part of the portfolio (providing a little diversification to my holdings). The biggest downside is the corporate governance issues which raises the first significant red flag.

Note that this information is dated to reflect their ownership as of Dec. 31, 2021. The numbers are likely a little different now as we are 7 months into the next year.

The phrase “limited” is going to vary based on the management of the company and the state of the economy.

You may stay away simply for this issue as it does create an incentive for something to be taken off the top. I would have no problem with such a decision, regardless of whether or not that is the same decision I would make.