Reviewing Cummins and Toro

Value Route and I Review CMI and TTC

Welcome, welcome, welcome. And a special shout out to our 10 readers. Yes, these are both some podcast jokes from Focused Compounding and Value After Hours. Seriously worth a listen if you haven’t checked out either.

Today we’re going to try something a little different. Please provide some feedback if you liked it, thought it could work with some tweeks, or just thought it was a waste of your time (really, it’s okay 😭😭…we can take it). Instead of just listening to me babble about some topic, I’m going to team up with Trevor Johnson (valueroute.substack.com) to talk about two brand name companies — Cummins, Incorporated (CMI) and The Toro Corporation (TTC). The idea is that these companies are closely related so some of the major concepts should apply to both. One thing that I want to stress is that as you’re reading this, assume that “we” are writing it as it truly is a joint collaboration.

Before I get too far though, let me say that the data provided here is from TIKR. They have a lot of data available on US and International Firms for prices that are quite a bit cheaper than your own Bloomberg terminal (as in a basic account for free and their most expensive account for $29.95 per month). With that said, let’s briefly introduce each.

Cummins Inc.

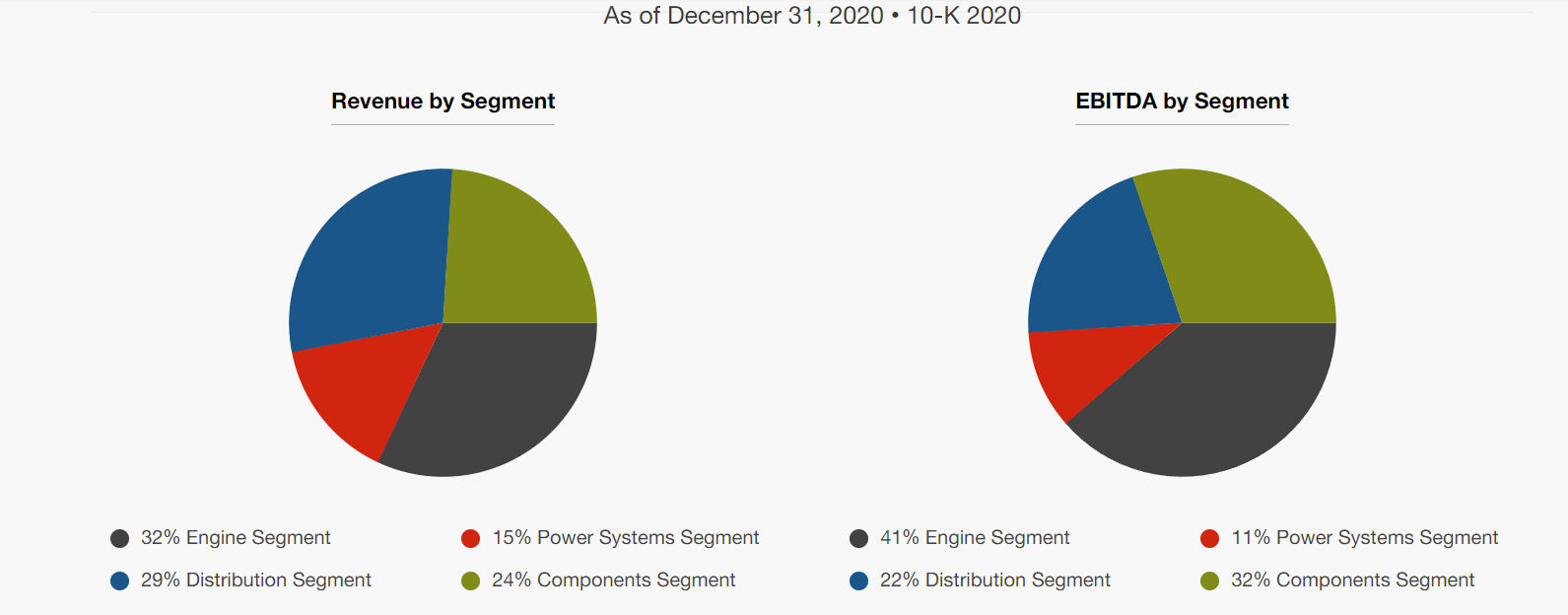

Cummins, Incorporated operates across five primary divisions — engine, distribution, components, power systems, and new power. The new power division is not yet profitable, and the rest have the following profitability levels.

They also have done a great job of generating ROIC over a longer time frame.

The Toro Company

The Toro Company produces products designed to help with landscaping/irrigation on the professional or personal level…but more professional. Specifically, they manage the following brands — Ditch Witch, Exmark, Boss Snowplow, American Augers, Ventrac, Subsite Electronics, HammerHead, and the list goes on. Heck, they even help manage the field at the 2022 Super Bowl — SoFi Stadium!

As you can see, they have a great record of profitability and Return on Invested Capital (ROIC).

Kevin on Valuation

We’re going to walk through a couple of valuation methods. My approach is relatively simple — A DCF model using the FCF estimates from TIKR for the next 5 years (2022 - 2026) plus a constant growth of 3%. I’m considering (a) that the next year’s FCF is going to be 2022 (we’re part way into 2022 for each firm, but it’s just a quarter for Toro and less than a full quarter for Cummins) and (b) that the required return is 8%. There are a few things that can change. One, you could argue that the FCF forecasts are either too optimistic or pessimistic. Two, you could argue that the required return should be greater than 8% or less than 8%. Finally, you could argue that the constant growth beyond 2026 should be more/less than 3%. All of these are legitimate arguments and we want to give you the ability to adjust these. So, first, here is the spreadsheet. Second, here is a video that walks through how to change each of these assumptions.

Trevor on Cummins

As pointed out above, $CMI’s business is split across five segments. These segments will shift as the years go on. Cummins management is confident in their ability to meet demand, whether that’s in traditional engines or zero emission/new power technologies.

Why is this important? Because the market might have Cummins all wrong. If you look at a one-year chart, the market has doubts that Cummins can properly make this shift. The stock over the past year has gone from ~$270 to ~$200, a decline of ~26%.

If we take a 10-year DCF and assume Cummins can get to ~$48B in revenue, the stock could be at a discount here:

If Zero Emission Vehicle adoption is quicker, as the right chart suggests, then revenue might be north of $50B. A model might look like this:

Ten years is a long way away and many things can change over that time. It becomes a bet on management that they are truly flexible like they say.

We could also be wrong on the margin assumption. Margins might look much different in an EV world vs traditional.

Let’s look at a bear case where revenue grows more in line with the economy and margins in an EV world are worse:

(Note: I left the terminal multiple the same in all for consistency. Realistically, it might be a little higher in the high growth scenario and lower in the low growth scenario.)

The 13x terminal multiple is around the mean of the past ten years:

Again, we want to give you the power to play around with these assumptions, so Trevor walks through how to change them to YOUR assumptions within the spreadsheet.

Trevor on Toro

Looking at Toro, they have a strong list of products for commercial (75% of their business) and residential (25% of their business). As mentioned above, Toro has a solid brand core. What’s next for Toro? A trend you’ll notice with all companies highlighted in today’s article is zero emission, battery powered, fuel efficient, etcetera. Toro specifically mentions all-electric equipment and smart solutions. One intriguing thing is the use of autonomous equipment. Toro wants to be a market leader in that category. They mention in their Q1 conference call an autonomous fairway mower that could help courses with labor shortages.

Toro will use new technology to help grow but what about the industries they will help? They point out Telecom (think fiber optics where you must dig, flow, move dirt), utilities and city infrastructure as growth opportunities. There is a question of how quickly businesses and individuals shift to new powered technologies. While Toro has adjusted by creating new products, they still benefit greatly from their gas product line. As more electric competition comes into play, does Toro lose any brand dominance?

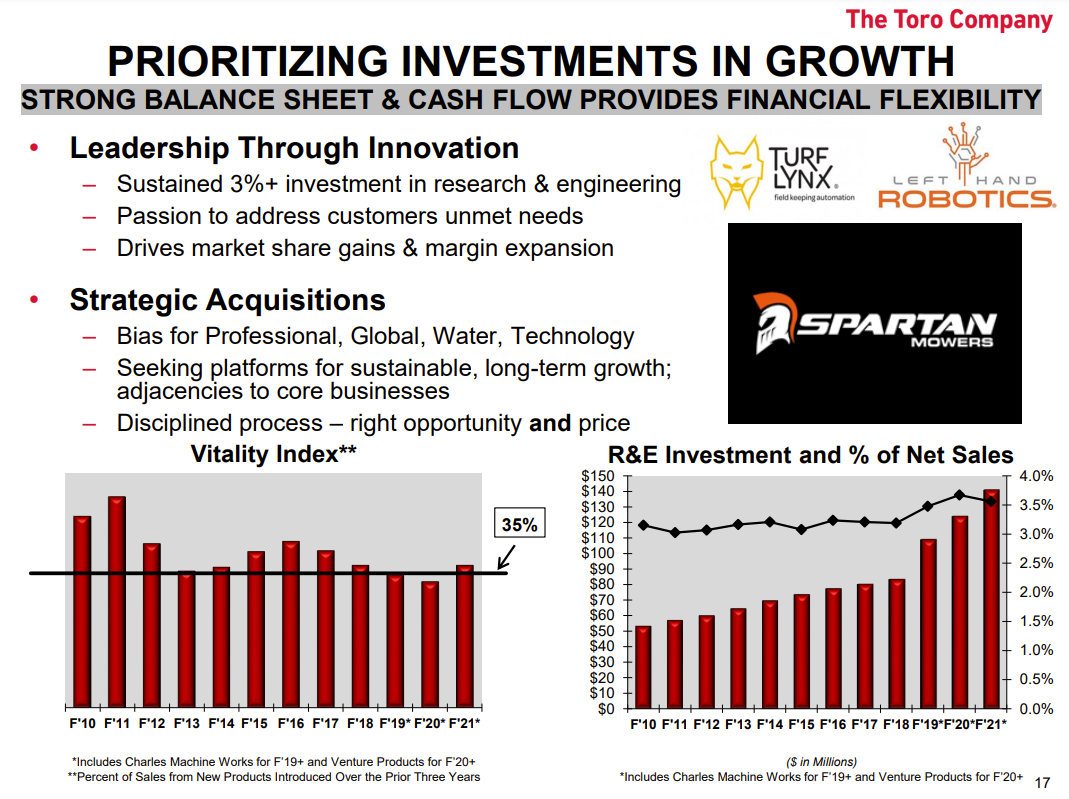

Snip from Toro’s Q1 slide deck highlights their investment decision process

While there looks to be a runway for revenue, margins are under pressure (specifically gross margin). Toro highlights higher material and freight costs as supply chain issues persist. The plus is they see these supply chain issues improving into the future as we continue to advance out of a COVID shutdown world.

If we assume Toro can get back to a normalized margin and revenue doubles in 10 years, here is what we get:

If we assume Toro’s growth runway is higher (Management is guiding 12-14% revenue growth this year. Some organic and some from a recent acquisition of Intimidator Group.) at 10% and margins normalize:

Let’s look at a gloomier outlook:

The point of this exercise is to test “what ifs” and what assumptions need to be made to justify the stock price today. Based on the assumptions above, you would need Toro to grow at a larger clip to invest here. Less enticing than Cummins.

General Discussion

In looking at these companies, Trevor and I decided that the approach should not be on trying to evaluate each business model and forecast from there. Each company has way too many businesses for that to be successful. Instead, we want to focus our attention on some of the themes these businesses face and talk a little bit about them. Specifically, we are going to discuss general demand for the products, the impact of Ukraine/Russia, and (most importantly) the transition to alternate energy souces.

Demand for Products

While these companies do not produce the same products, there is some overlap in that they are both industrials. Cummins targets the on/off highway market (primarily engines, components, and distribution) while Toro targets landscaping equipment (mowers, irrigation, snow removal, digging, etc.). If we think of demand for these products, it is expected to be positive (5-10% per year) for the next few years. That said, each of these companies is dependent on costs which are also expected to be facing some pressures in the near term (especially with the Ukraine/Russia situation under way — which we will address shortly). While we wouldn’t classify demand for production as “through the roof”, I think we would both classify it as a little higher than GDP growth for the next five years.

Trevor makes an excellent point that both of these companies have been around for over 100 years (Cummins is the “new” guy as they started in 1919 while Toro has been around since 1914). Despite their age, they are also still growing quite well. While there are areas where new startups have tremendous power (they can reinvent themselves from scratch because that’s were they are starting from). With brands, there is a big advantage to having staying power and reputation that comes from surviving multiple downturns and building important relationships with clients.

Impact of Ukraine/Russia

Obviously Ukraine/Russia is going to impact these companies. Probably the company that will be most impacted is Cummins. Last year, they did $675 million in the areas that are impacted by the Russian crisis relative to their $25.5 billion overall. Granted, this is purely revenue, so their costs will drop along with their revenue and it assumes that the revenues will be gone all year (which at this point seems reasonable). Either way, I think we can assume that it is going to cost them some of their revenue/profits, but overall it is likely going to be small. It also may impact them due to commodity price fluctuations.

Toro is in much better shape. They do no have any manufacturing plants in Ukraine/Russia and 80% of their revenues come from the United States. It is possible that there could be some revenue impact if the conflict were to expand significantly, but as of now it doesn’t appear to be a major influence on revenues. Where it could have an impact is on commodity prices that are used as inputs on the products that they produce.

Transition to Alternate Energy

One of the more obvious challenges facing each of these companies is that the world is moving away from internal combustion engines (ICE) to electric energy as it is has significant advantages for the environment. There is a significant question regarding where the energy ultimately comes from (solar, wind, coal, hydro, etc.) and how strong our power grid is (think brownout conditions). However, I think it is smart for firms to be thinking about how they are going to make the transition in a market-based dynamic. Fortunately, each of these firms is doing this.

Toro is developing their HyperCell Battery Management System. In addition, the comment came up in their recent quarterly call about Home Depot testing 50 stores with no gas powered outdoor equipment. That is obviously a pretty big test which is likely being done to see if there is enough demand to expand the solution. Fortunately, Toro appears to be ready.

Renee Peterson

And keep in mind, with the 60-volt, we've really expanded our product line. So we're in some other adjacent categories that we weren't in before. So it's certainly beyond the mowers and snow blowers, which we do have strong product offerings in, but we have a lot of other products that we sell as well, too.

Richard Olson

Right. I think the really astonishing thing is just where we circle back and where we were offering battery solutions, for example, in the snow categories, we just double or triple down on our reputation and brand and the features that we have that are independent of the power source. So where we start to offer incredibly viable products that work exceptionally well that are battery. All of a sudden, the customers get the benefit of our expand sort of network both mass and dealer-oriented. So the access to us from a servicing standpoint and just the reputation in snow -- the reputation that's really earned by the features, the benefits, the innovations and the customer experience that you're going to get with the Toro product.

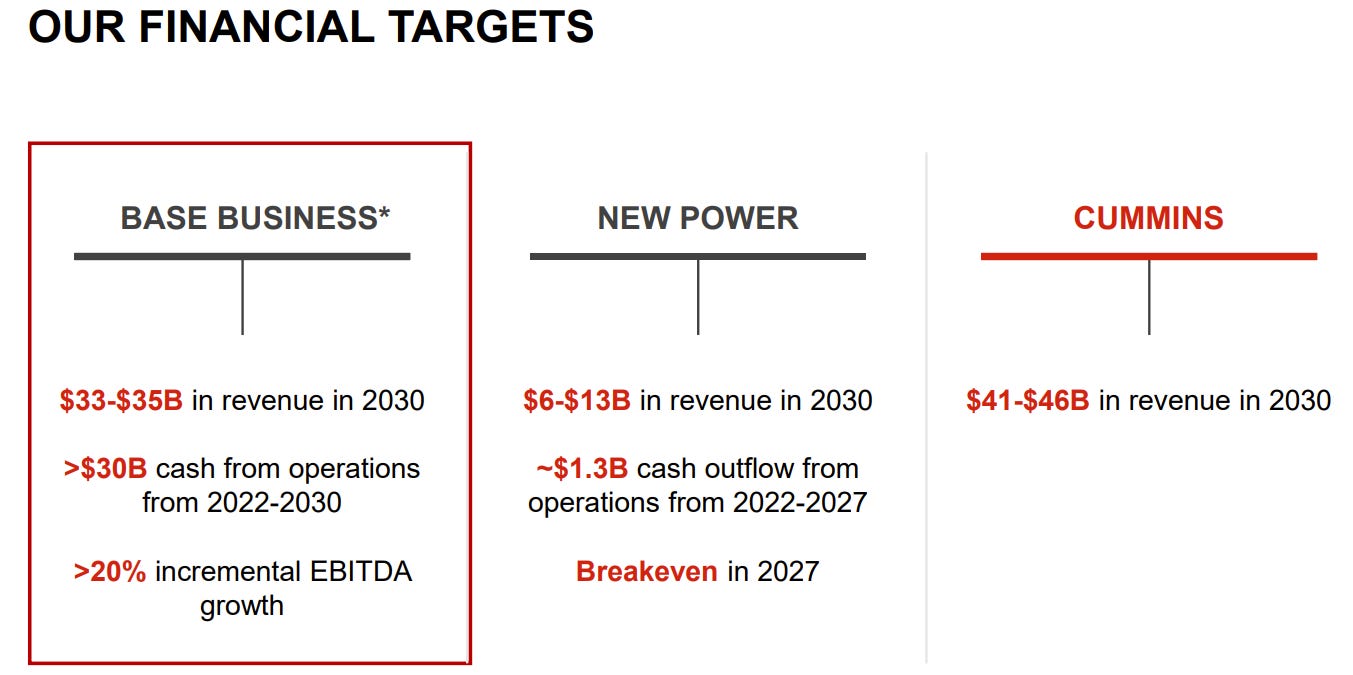

Cummins is also stressing the move to it’s New Power division. Trevor mentioned this earlier in his valuation analysis of CMI with their focus on alternative energy. They know that the market is not there yet, but that there is significant demand from investors, both at their firm and those of firms that they work with, to address the potential climate change issue. Importantly, they know that (a) they can’t just flip a switch to adjust — it takes time, money and (most importantly) technology to make conversion efficient and (b) that the firms they sell stuff to are interested, but also need it to make sense from an economics perspective. Therefore, they have started their New Power division and expect to reach breakeven in 2027 before turning profitable. Granted, it may be a year sooner or two years later, but they at least are planning for the future.

Wrap Up

A quick wrap up is that both Cummins and Toro are attractive brand names that have consistently earned a higher ROIC than their cost of capital. They have a long history and are working on addressing their response to climate change. These are all positive traits, but ultimately a big part comes down to how expensive the stock is. We walk through a couple of valuation models, but more importantly provide the tools for you to modify these spreadsheets to create your own valuation models. Don’t like our assumptions? Change them to your assumptions!

Special shout out to Value Route for his help in putting this Substack together. Did you like it? If so, hit the like button or, better yet, leave a comment and tell us what you liked (or didn’t like) so we can work on making it better.

| A guest post by

|