More Positions

Cancer Update #4

Not too much new to report. I’ve completed two weeks of the radiation and chemotherapy treatment (4 weeks to go on the radiation). So far, nothing really to report other than a slightly foggy head for a bit plus a light radiation “burn” (very light) along the radiation treatment. The chemotherapy is simply taking a pill in the morning and then laying back down for an hour or two…I think I can handle that!

So far, it’s really progressing about as well as one could imagine, so 👍👍!

Cigarette Positions

I have a couple of cigarette positions which I’ll go through. First, let me throw out the disclaimer. These are ethically borderline calls and I completely respect those who choose to stay away. I mean the product will literally kill you if you use it, so it is hard to defend from that standpoint. However, my job as an investor is to find assets that are undervalued for a reason. With cigarettes, the reason is simple — too many people won’t invest in them which leads to an undervalued asset (and it will stay undervalued as I don’t see the plot twisting anytime soon). So, cigarettes are dangerous. So is speeding, drinking alcohol, not getting a COVID vaccine, and a lot of other behaviors. My job is not to set behavior (it can’t happen), but to invest in a way that will make me a positive risk-adjusted return.

Altria (MO)

This is one of my larger positions with about $65,000 of my portfolio. The reason I like it is that it pays a 7.15% dividend and generates an 8.9% FCF yield. Both of these are reasonable returns. There is also very little competition coming in due to restrictions on investing in the business. However, there may be new competition coming from another smokable product — cannabis. This is in the “grey” zone now (although give it a few years and the “grey” should turn a lot clearer). Just like sports gambling is becoming legal in more places, so to should cannabis. The challenge is that legal on the state level is not the same as legal at the Federal level…at least for now. I’ll talk a little more about my cannabis investments in a bit.

British American Tobacco (BTI)

This is another of my tobacco positions with a high dividend yield of 6.9% and 10.9% FCF yield. Both of these are solid returns ignoring any capital gains, but should also see EPS growth of about 4-5% per year going forward. There is little chance of seeing 20%+ returns, but also little chance of seeing -10% returns going forward. This one accounts for about $43,000 of the portfolio.

Philip Morris International (PM)

This is the “pricey” of my tobacco positions and accounts for about $32,000 in my portfolio. When I say pricey, it implies that it has a dividend yield of only 4.9% and a FCF yield of 6.6%. Neither of these are at quite the level of Altria or British American Tobacco, but are still reasonable. However, the growth is expected to be a little bit higher going forward (5-10%) in EPS and FCF going forward.

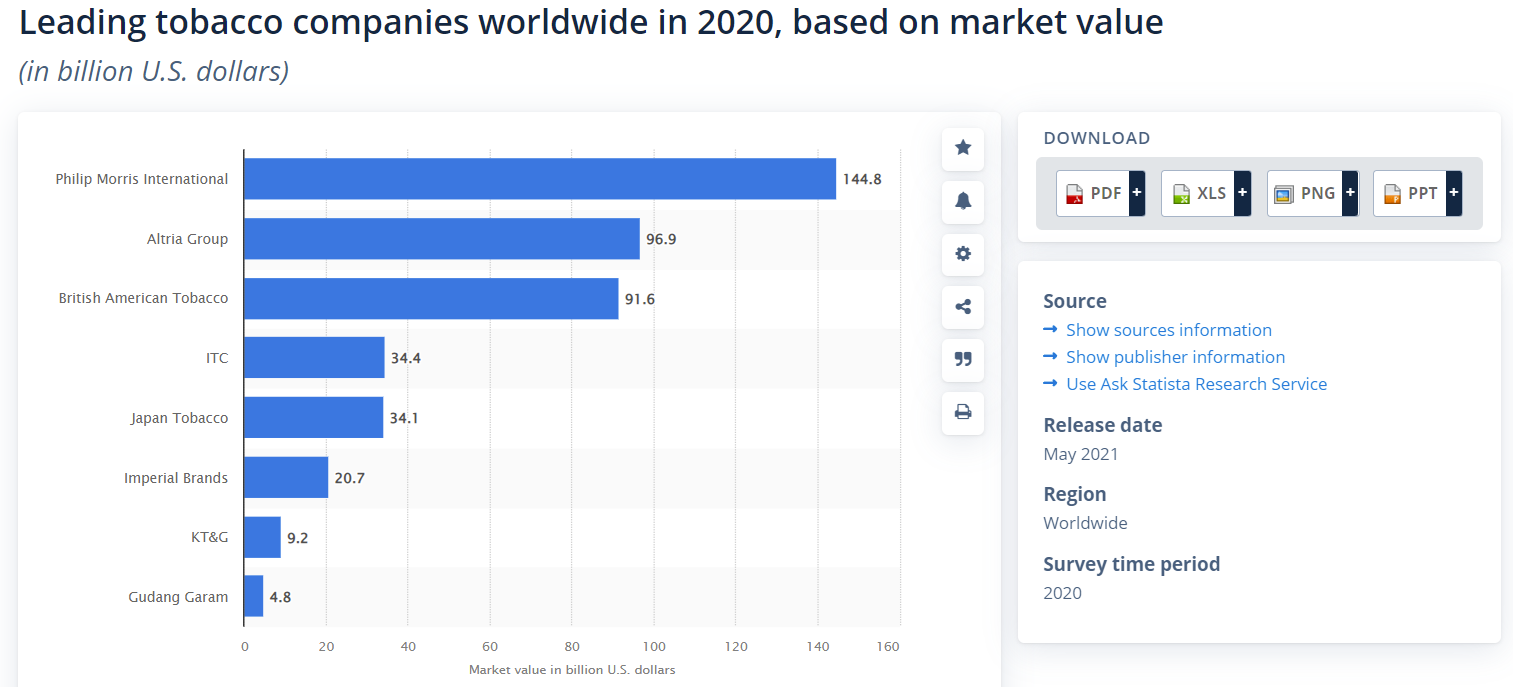

According to Statista, these are by far the three largest tobacco companies as of 2021 which provides some reasonable coverage. My plan is to hold and reinvest dividends over the upcoming years. All told, that represents about $140,000 of my portfolio.

Cannabis Lottery Tickets

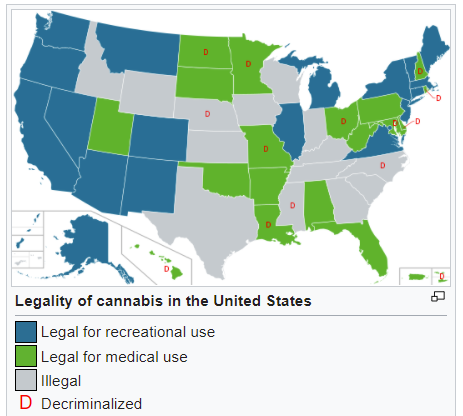

This is one of those positions that I’m playing back and forth in my mind. On one hand, there is a lot to like about cannabis. First, there is a Wild West mentality in the cannabis sector where we have lots of players and don’t know who is going to end up on top. IF (a very big if), things break right, we have potential for stocks to go up by 5X-10X over the next 10 years. For that to happen, cannabis needs to be legalized (a big question mark, but trending in the right direction) at the federal level. What we have now “works” in that cannabis is legal in certain states (18 states plus the District of Columbia) for recreational use and even more states (36 states plus the District of Columbia) for legal use with medical prescription. On a geographic basis, it is mostly legal along the West coast and in the Northeast.

So, let’s talk about SAFE (Secure and Fair Enforcement) Banking Act. It has been muddling it’s way through Congress. According to Wikipedia, the current version of SAFE:

This bill generally prohibits a federal banking regulator from penalizing a depository institution for providing banking services to a legitimate cannabis-related business. Prohibited penalties include terminating or limiting the deposit insurance or share insurance of a depository institution solely because the institution provides financial services to a legitimate cannabis-related business and prohibiting or otherwise discouraging a depository institution from offering financial services to such a business.

Additionally, proceeds from a transaction involving activities of a legitimate cannabis-related business are not considered proceeds from unlawful activity. Proceeds from unlawful activity are subject to anti-money laundering laws.

Furthermore, a depository institution is not, under federal law, liable or subject to asset forfeiture for providing a loan or other financial services to a legitimate cannabis-related business.

The bill also provides that a federal banking agency may not request or order a depository institution to terminate a customer account unless (1) the agency has a valid reason for doing so, and (2) that reason is not based solely on reputation risk. Valid reasons for terminating an account include threats to national security and involvement in terrorist financing, including state sponsorship of terrorism.

Finally, the bill decreases the cap on the surplus funds of the Federal Reserve banks. (Amounts exceeding this cap are deposited in the general fund of the Treasury.)

In other words, SAFE Banking Act makes cannabis effectively legal and allows participants to engage in financial market transactions and participate in banking activities. According to Ed Perlmutter, the current laws are a bit outdated:

Therefore, businesses that legally grow, market or sell cannabis in states that have legalized its sale are generally locked out of the banking system, making it difficult for them to maintain a checking account; access credit; accept credit and debit cards; meet payroll; or pay tax revenue.

Clearly, we can see that SAFE Banking Act is a necessity to have physical cannabis shops operate in a “normal” environment. It is NOT necessary to see them operate in a “non-normal” environment, but one in which payment systems are much stricter and, therefore, more expensive. While SAFE Banking Act has passed the US House five times, it has not had a run in the US Senate.

Another important topic relates to health impact. Here, the Cato Institute has a study out that indicates:

Limited post-legalization data prevent us from ruling out small changes in marijuana use or other outcomes. As additional post-legalization data become available, expanding this analysis will continue to inform the debate. The data so far provide little support for the strong claims about legalization made by either opponents or supporters.

A final topic has to do with impact on illegal cannabis competing against legal cannabis. This story was covered in tremendous detail in Politico here (‘Talk About Clusterf---’: Why Legal Weed Didn’t Kill Oregon’s Black Market) so I won’t go into the details. However, one of the strong arguments for legalization is to eliminate the need for illegal drugs. As you can see, this is not working out exactly as planned. A big reason for this is likely related to the high levels of taxation on cannabis. You can get a feel for tax law based on this handout from TaxAdmin.org…it’s not cheap. Plus it varies quite a bit from one state to the next.

However, all of this creates the opportunity. Right now, legal cannabis sales are only available through Canadian shares and Over-the-Counter markets (the positions I have are all OTC stocks), along with ETFs. This means that supply of shares is relatively limited and the grey market attitude of the stocks makes their legal nature less understood. At this time, there is a good reason for institutional investors to keep their hands off, but also a good reason for individual investors (who don’t always make good decisions) to try to time the market. Which makes this a confusing ball of wax to investors like me who (a) are interested in the potential switch and increased confidence but are also (b) not sure how much should be put into a bet that is speculative at best (and speculatively bad at worst). If you have some thoughts on the cannabis positions, I’m all ears!

Glass House Brands

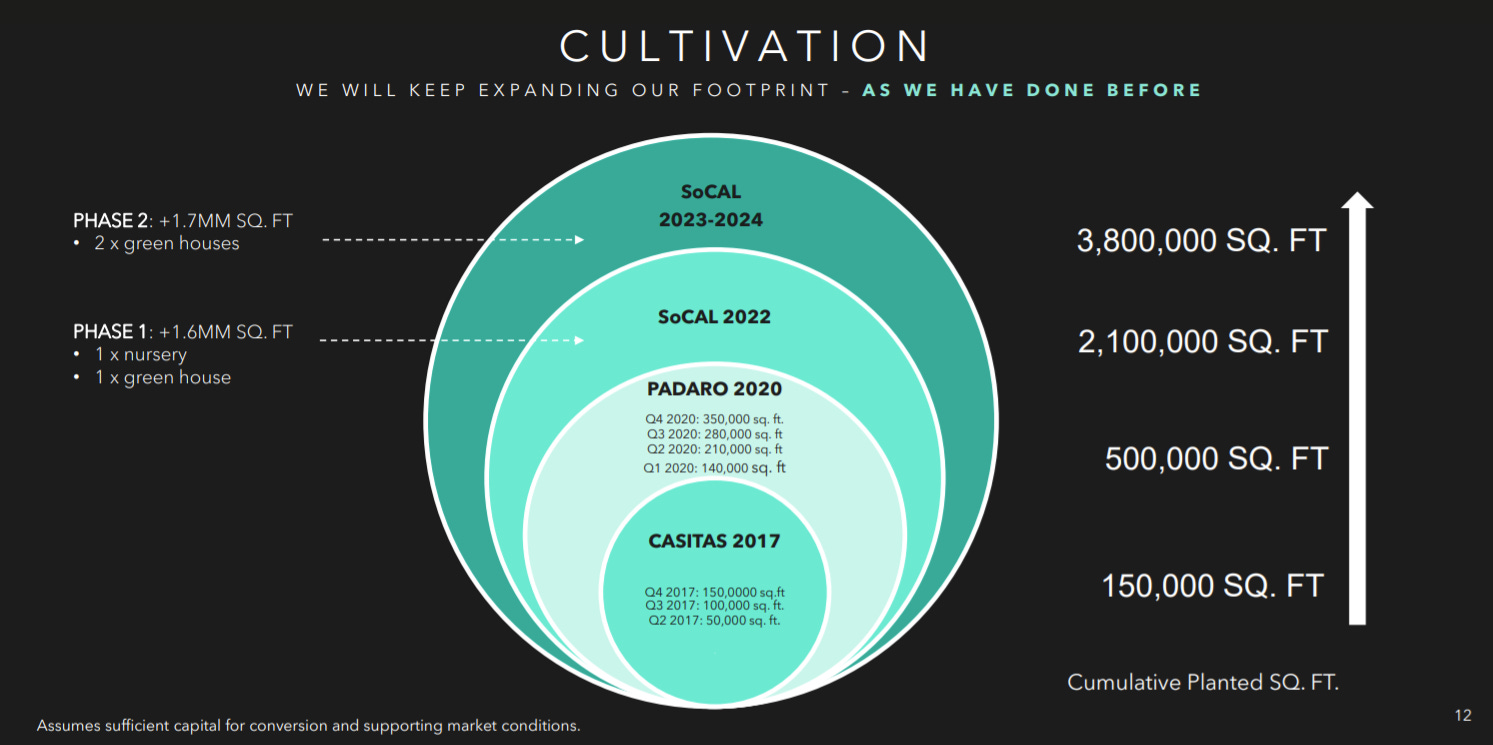

This is one of my “bigger” positions (and is still pretty small) at just under $15,000. Right now, Glass House is bleeding cash (not good), but my bet is that this is going to turn around before too long. They are starting with a huge net loss (-$25 million) and getting FCF back to -$12 million. Plus, they’re CF from Investing Activities is also a huge outflow (-$98 million). All of this is far from the highlight. Instead, what makes them attractive is that they are building a really large (as in over 100 football fields) greenhouse to grow cannabis. Yes, they are betting on it growing and preparing for that growth! This should bring their cultivation costs to $226/lb (give or take).

Verano Holdings (VRNOF)

Verano Holdings is another very small bet on the cannabis sector with only about $7000 (a little under) in holdings. This is a FCF positive company (and has been for awhile) with $35 million (from a base revenue of $207M in the 3rd quarter). They currently have 89 operations across 15 states. Granted, their total Enterprise Value is relatively high at 4.2X revenues, but their growth should make that very attractive over the next few years.

MSOS ETF (MSOS)

This is an ETF whose strategy is to own a large mix of diversified holdings. Their largest holdings include Green Thumb, Innovative Industrial (more on this in a minute), Trulieve, Curaleaf and Cresco Labs. This is a relatively high fee fund (0.73%) which is a strike against it. Granted, in the short-run, not a big deal. Over 20+ years, a much bigger deal (we’ve talked about costs before). The idea here is to just get a basket of cannabis companies. This is another smallish position at $8400.

Innovative Industrial Properties (IIPR)

This is one of my original (purchased back in 2018 for $28 per share) and held since then…it currently trades for $189. Which sounds good until you realize it traded for $286 at it’s peak. Granted, it is a smallish position (only 194.83 shares…100 of which were purchased and the rest from the dividend reinvestment program) for $22,000. However, it has been one of the better investments (purely from dumb luck) that I have had.

That puts me at about $30,000 in straight cannabis positions and $52,000 in total cannabis positions. These represent 1% of my portfolio (just counting the pure cannabis…IIPR is not truly a cannabis position). Is it too small? The right size? I’m not sure. I like that it is a restricted arena, but there is a lot of risk involved as well. Again, feel free to offer some feedback on this if you have any.